I have been horrible at keeping up with this blog lately, mostly because I do no good and nothing has really changed for the better. Maybe if I had kept up with it, I would show a little more restraint, but I haven't so here we are.

First, a little level setting. At a point earlier this year, our overall debt had decreased to $200,713.01. We had four credit cards with a combined balance of a little more than $27,000. We also had two car loans with a combined outstanding debt of $29,064, and my student loans with an outstanding balance of $39,766. We also had a mortgage loan of $104,678.

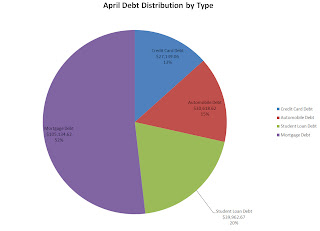

As of the end of November we had $202,346.77 in debt. It is more now, but I don't have actual totals at the moment. Of that debt, $29,227 was on credit cards, $26,934 was for cars, $39,645 was for student loans, and $106,539 was for our mortgage. So, our credit card debt went up more than $2000, our cars went down a little more than $2000, student loans stayed stagnant, and the mortgage debt actually went up as a result of our refinancing.

Clearly, this does not reflect well on my money management skills.

In addition to increased debt, we now carry balances on all of our credit cards. Not just balances, actually, high balances. Nearly maxed out and juggling the cards to avoid going over the limit or being declined for a purchase. It is mostly because of our Disney trip last month, and because of Christmas shopping this month (which we did spend significantly less this year than we have in years past), but also because we want what we want when we want it.

I had planned to pay my Discover Card off in March, when I received my performance bonus, by not using the card in the interim and paying more than the minimum payment every month. Instead, we use the Discover Card regularly and carry a high balance. I was juggling all of our finances, trying to figure out how we could pay the entire balance off before it starts accruing interest and not completely destroy ourselves financially. As more and more minimum payments started rolling in, the picture was actually pretty bleak, with me feeling like my only option would be to drain the kids savings accounts and my savings account to pay it. Even then, it was going to be tight.

In addition to the Discover Card, I had it all budgeted out how I was going to pay my Best Buy card off two months later, then my credit union credit card, and then my student loans. I was going to systematically pay off all of my debt by next summer by snowballing payments and going smallest balances first (with the exception of the Discover Card and Best Buy card because they both had promotional interest rates that were expiring). We would have paid off all of our credit cards by next July and one of our cars by the end of next year. We'd be saving for a house and probably able to handle two mortgages.

Except for that pesky problem of spending money. How are we ever going to get ahead when we're spending so much on credit card payments that we don't ever have any extra? But it never stopped us from spending the money anyway. I was starting to feel the walls closing in and feeling the panic that we weren't going to be able to pay our bills when we started paying interest on an $11,000 credit card.

And then today happened.

Today, I was offered a new job. I had applied for it at the beginning of November and hadn't heard anything before we went to Disney. I got back from our trip and had a voicemail inviting me to interview for the position. I interviewed last week and, because it was in my current office, got a feel for where they were headed in the hiring process. Even though the majority of this job was stuff I'd already been doing, I was one of two top candidates for the position. The other possessed a technical skillset that I lack, but I have my own technical skills and experience with the responsibilities of the role. I was on pins and needles waiting for a decision, and the longer it dragged out, the more convinced I became that they had decided to go with the other candidate. Instead, I was called into the hiring managers office this morning and offered the job, and a more substantial raise than I ever could have imagined.

I came home this evening and put the numbers into the paycheck calculator. The number that was spit back at me made me do a double take and I ran the numbers again. Nope, that was right. More than $400 extra. Per paycheck. Every two weeks. Over $800 more a month than I currently take home. I plugged the numbers into my budgeting spreadsheet (as savings, not spending money) and there it was... the answer to our downward spiral. With this influx of income, even if - if - we maintain the maximum balance on the Discover Card, we will have enough in savings by March to pay the entire balance, in full. After that, the other credit cards start falling off quickly The small balances disappear in a couple of months and the big balances will be gone by year end.

If we continue to budget based on my current salary, our credit card debt will be nonexistant by this time next year. If we don't spend the extra money on anything except debt payment. If we've survived this long, surely we can do it for another year. And then a year from now, we can just start socking money away in savings and maybe even investments. Maybe buy a house we don't hate. This promotion, doing something that I actually enjoy, and the raise that came with it just dramatically changed the path our lives were on. I can't wait for everything to start turning around. This might just be the boost we need to get ourselves under control.

Wednesday, December 19, 2012

Wednesday, October 10, 2012

I Get Knocked Down.... Do I Get Up Again?

My husband and I lack self control. We can't stop spending money. We get ahead, we spend the money, we get back down.

We're going to Disney next month and I'm ridiculously excited about it, but we went overboard booking the hotel I wanted with the view that I wanted during the week that I wanted. But it came with a price tag that is a lot more than we've ever spent on a vacation. Yesterday was our last day to get a full refund on the price, so of course today, my employer decided to burst my bubble.

I budget. A lot. I have our bills mapped out through the next year. I always estimate a $20 biweekly increase in health insurance premiums during annual enrollment because, on average, that's what it's been. Last year, I think it went up $19. Today, I found out that our insurance is going up $37 per pay next year. In addition to that, because my husband is eligible for coverage through his employer, they are going to charge me $50 per pay as a surcharge because he is using my insurance coverage and not his own.

I have some massive, massive issues with this. First and foremost, my company blamed this surcharge on the Affordable Care Act (ACA), or "Obamacare" as it's been dubbed by the media and politicians. I whole-heartedly disagree. If the surcharge had anything to do with ACA, then it would have been implemented across the entire company. Which leads me to point number two...

This surcharge is only being assessed on employees whose spouses 1) work and 2) don't work for our company. So essentially my company is targeting those employees who have two incomes, one of which doesn't come from our company. No other segment of the company is facing this increase.

If the increase legitimately had anything to do with healthcare reform, it would have impacted everybody. Instead, I am left feeling like my company could care less about people and especially about families.

The increase, between increased premiums and the surcharge, will be taking 5% of my salary. 5% is a pretty substantial amount, especially when we have two incomes because we have to, not because it's a luxury. I will actually make less next year than I am this year because of this increase; the average raise in the spring is about 2%.

Our budget is stretched thin, literally down to pennies left after paying bills, through most of next year. I don't know how we're going to find an extra $87 every two weeks to pay for health care.

We're left with a couple of options, none of which are very desirable.

1) I keep my husband on my insurance. I pay an extra $87 every two weeks for his insurance coverage, which he has never used. Not once.

2) I drop my husband from my insurance and make him get his own. We pay two premiums, and are responsible for two deductibles if my husband ever has to seek out medical care. We have to juggle two different insurance companies, make sure that any doctor we choose accepts both companies. The list of reasons that this is an undesirable option goes on and on.

3) I drop my husband from my insurance and he stays uninsured, paying the tax for not maintaining coverage. In the event of catastrophic illness, we're screwed.

Clearly, none of these are attractive options. My company has put me and my family in a really bad position.

Today, I just feel like giving up. I'd be better off to quit my job and get Medicaid. I don't know why I try to get ahead when everything in the world is just trying to drag me down.

We're going to Disney next month and I'm ridiculously excited about it, but we went overboard booking the hotel I wanted with the view that I wanted during the week that I wanted. But it came with a price tag that is a lot more than we've ever spent on a vacation. Yesterday was our last day to get a full refund on the price, so of course today, my employer decided to burst my bubble.

I budget. A lot. I have our bills mapped out through the next year. I always estimate a $20 biweekly increase in health insurance premiums during annual enrollment because, on average, that's what it's been. Last year, I think it went up $19. Today, I found out that our insurance is going up $37 per pay next year. In addition to that, because my husband is eligible for coverage through his employer, they are going to charge me $50 per pay as a surcharge because he is using my insurance coverage and not his own.

I have some massive, massive issues with this. First and foremost, my company blamed this surcharge on the Affordable Care Act (ACA), or "Obamacare" as it's been dubbed by the media and politicians. I whole-heartedly disagree. If the surcharge had anything to do with ACA, then it would have been implemented across the entire company. Which leads me to point number two...

This surcharge is only being assessed on employees whose spouses 1) work and 2) don't work for our company. So essentially my company is targeting those employees who have two incomes, one of which doesn't come from our company. No other segment of the company is facing this increase.

If the increase legitimately had anything to do with healthcare reform, it would have impacted everybody. Instead, I am left feeling like my company could care less about people and especially about families.

The increase, between increased premiums and the surcharge, will be taking 5% of my salary. 5% is a pretty substantial amount, especially when we have two incomes because we have to, not because it's a luxury. I will actually make less next year than I am this year because of this increase; the average raise in the spring is about 2%.

Our budget is stretched thin, literally down to pennies left after paying bills, through most of next year. I don't know how we're going to find an extra $87 every two weeks to pay for health care.

We're left with a couple of options, none of which are very desirable.

1) I keep my husband on my insurance. I pay an extra $87 every two weeks for his insurance coverage, which he has never used. Not once.

2) I drop my husband from my insurance and make him get his own. We pay two premiums, and are responsible for two deductibles if my husband ever has to seek out medical care. We have to juggle two different insurance companies, make sure that any doctor we choose accepts both companies. The list of reasons that this is an undesirable option goes on and on.

3) I drop my husband from my insurance and he stays uninsured, paying the tax for not maintaining coverage. In the event of catastrophic illness, we're screwed.

Clearly, none of these are attractive options. My company has put me and my family in a really bad position.

Today, I just feel like giving up. I'd be better off to quit my job and get Medicaid. I don't know why I try to get ahead when everything in the world is just trying to drag me down.

Monday, July 23, 2012

July Update

I haven't gotten back to write like I keep telling myself that I'm going to. This month has been kind of crazy with everything that has been going on.

I did consolidate my student loans, and when I got the new loan amount, it looks like they did not apply my June payment. I contacted Mohela about it several weeks ago and did not get a response, so I have asked for a copy of my payment history in hopes that I can see actual amounts of my loans at the time of consolidation. I did not expect that Mohela would delete my loan history from their website as soon as the loan was consolidated, so I foolishly did not print off my summary sheet before the consolidation occurred. Direct Loan Servicing is no help because they weren't servicing the loan at that time and Mohela has been no help because they are unresponsive.

I ended up changing the repayment plan to the graduated repayment plan because it reduced my payments $60 a month and only added about $500 extra interest to the total cost of my loan. I plan to put the difference towards higher interest credit cards, which we are still on target to pay off next year. My husband also got a bonus in this paycheck, so that will help.

We are still waiting on our refund from the county auditor, from where they lowered the value of our house for 2010 and 2011. Based on approximate taxes for our value, we should be receiving about $500 or $600 back. The county said it would be approximately 60 days, but did not clarify whether it would be 60 days from the decision, or 60 days from the date they responded. Either way, I still have not seen the updated value reflected on their website and it's been about 90 days since the decision was made. I guess it's time to harrass them again. You know they would not be as understanding if I were late on my tax payments.

We're also still wrapped up in the nightmare that is refinancing our home with US Bank.

We applied for the refinance in April and were told that we would be under a 90 day ratelock, but that generally the refinances were processed within about 60 days. I received the application paperwork and returned it, along with all supplemental documents requested. A week or so later, I was told that, although I had submitted the signed paperwork to request a transcript of my previous two years tax returns and my previous two years W-2's, they now needed a copy of my actual tax return. I was angry. ANGRY. Because they hadn't requested these documents at the time we were applying, so I felt they were just delaying the refinance process, and because they already received the information from our tax transcripts, so I felt like they were... I don't know, trying to catch us in a lie? I'm not sure. I returned the tax returns anyway and they responded back that they needed all of the supporting pages. Um, why?? Like most normal individuals in the 21st century, I filed electronically, with documents that were provided to me electronically. I had already printed off the electronic copies of my tax returns and signed them, backdating them more than a year, and now I was trying to gather other supporting documents. US Bank seriously, SERIOUSLY needs to update their processes for modern technology.

Anyway, all of the documents were finally received by US Bank, it went through underwriting and was in scheduling when our area was hit by strong storms, bringing strong winds, hail, power outages, etc. A few days later, we got a call from US Bank that our refinance had been pulled back from scheduling because we were now being subjected to a driveby inspection to ensure that our home was still standing and had not been damaged. I was annoyed, but understood.

Last week, we got a phone call from an appraisal company wanting to schedule an appraisal. I was taken by surprise because we had been told two months ago that we would not need an appraisal because they were using automated values. I went ballistic. I called US Bank and our loan processor was out of the office for the week, I complained on their facebook page, I got ahold of a supervisor who told me it was their direction that everybody within the affected area had to have a full appraisal. The more I thought about it, the more angry I got, so I complained further about how we'd been jerked around with all of the additional paperwork after we started the application process and now, because of their incompetence we were going to be subjected to an appraisal that was going to cost us an additional $400 because they dragged the process out so long. I got another phone call from the supervisor indicating that the appraisal was required by Fannie Mae, who backs our mortgage. The thing is, I have a coworker who is refinancing with her loan held by Fannie Mae and she is not being subjected to an appraisal, so I think US Bank is full of it.

Anyway, the appraiser came out on Wednesday and was there for less than 10 minutes. The US Bank supervisor told me we needed to be at $88,000 for the value of our home. It came back at $85,000. She indicated that the difference in value did not impact our refinance, so we will be moving forward and closing next week. I will be glad to see the drop in payment, even though I know the majority of the drop is because we're going back to a 30 year loan. My hope is, with the way property values have been increasing in our neighborhood, we will get close to breaking even by next year. I don't mind taking a small loss, as long as it doesn't break us. We're hoping with the opening of a casino a few miles down the road, that our property will see a dramatic increase in value late this year and early next.

We're going to use the reduction in mortgage payment to pay down credit card debt, and then probably put half towards paying down principle on this loan and half towards saving for a down payment on a new home. We're getting closer to being on level footing and getting ourselves out from under the mountain of debt we have accumulated.

I did consolidate my student loans, and when I got the new loan amount, it looks like they did not apply my June payment. I contacted Mohela about it several weeks ago and did not get a response, so I have asked for a copy of my payment history in hopes that I can see actual amounts of my loans at the time of consolidation. I did not expect that Mohela would delete my loan history from their website as soon as the loan was consolidated, so I foolishly did not print off my summary sheet before the consolidation occurred. Direct Loan Servicing is no help because they weren't servicing the loan at that time and Mohela has been no help because they are unresponsive.

I ended up changing the repayment plan to the graduated repayment plan because it reduced my payments $60 a month and only added about $500 extra interest to the total cost of my loan. I plan to put the difference towards higher interest credit cards, which we are still on target to pay off next year. My husband also got a bonus in this paycheck, so that will help.

We are still waiting on our refund from the county auditor, from where they lowered the value of our house for 2010 and 2011. Based on approximate taxes for our value, we should be receiving about $500 or $600 back. The county said it would be approximately 60 days, but did not clarify whether it would be 60 days from the decision, or 60 days from the date they responded. Either way, I still have not seen the updated value reflected on their website and it's been about 90 days since the decision was made. I guess it's time to harrass them again. You know they would not be as understanding if I were late on my tax payments.

We're also still wrapped up in the nightmare that is refinancing our home with US Bank.

We applied for the refinance in April and were told that we would be under a 90 day ratelock, but that generally the refinances were processed within about 60 days. I received the application paperwork and returned it, along with all supplemental documents requested. A week or so later, I was told that, although I had submitted the signed paperwork to request a transcript of my previous two years tax returns and my previous two years W-2's, they now needed a copy of my actual tax return. I was angry. ANGRY. Because they hadn't requested these documents at the time we were applying, so I felt they were just delaying the refinance process, and because they already received the information from our tax transcripts, so I felt like they were... I don't know, trying to catch us in a lie? I'm not sure. I returned the tax returns anyway and they responded back that they needed all of the supporting pages. Um, why?? Like most normal individuals in the 21st century, I filed electronically, with documents that were provided to me electronically. I had already printed off the electronic copies of my tax returns and signed them, backdating them more than a year, and now I was trying to gather other supporting documents. US Bank seriously, SERIOUSLY needs to update their processes for modern technology.

Anyway, all of the documents were finally received by US Bank, it went through underwriting and was in scheduling when our area was hit by strong storms, bringing strong winds, hail, power outages, etc. A few days later, we got a call from US Bank that our refinance had been pulled back from scheduling because we were now being subjected to a driveby inspection to ensure that our home was still standing and had not been damaged. I was annoyed, but understood.

Last week, we got a phone call from an appraisal company wanting to schedule an appraisal. I was taken by surprise because we had been told two months ago that we would not need an appraisal because they were using automated values. I went ballistic. I called US Bank and our loan processor was out of the office for the week, I complained on their facebook page, I got ahold of a supervisor who told me it was their direction that everybody within the affected area had to have a full appraisal. The more I thought about it, the more angry I got, so I complained further about how we'd been jerked around with all of the additional paperwork after we started the application process and now, because of their incompetence we were going to be subjected to an appraisal that was going to cost us an additional $400 because they dragged the process out so long. I got another phone call from the supervisor indicating that the appraisal was required by Fannie Mae, who backs our mortgage. The thing is, I have a coworker who is refinancing with her loan held by Fannie Mae and she is not being subjected to an appraisal, so I think US Bank is full of it.

Anyway, the appraiser came out on Wednesday and was there for less than 10 minutes. The US Bank supervisor told me we needed to be at $88,000 for the value of our home. It came back at $85,000. She indicated that the difference in value did not impact our refinance, so we will be moving forward and closing next week. I will be glad to see the drop in payment, even though I know the majority of the drop is because we're going back to a 30 year loan. My hope is, with the way property values have been increasing in our neighborhood, we will get close to breaking even by next year. I don't mind taking a small loss, as long as it doesn't break us. We're hoping with the opening of a casino a few miles down the road, that our property will see a dramatic increase in value late this year and early next.

We're going to use the reduction in mortgage payment to pay down credit card debt, and then probably put half towards paying down principle on this loan and half towards saving for a down payment on a new home. We're getting closer to being on level footing and getting ourselves out from under the mountain of debt we have accumulated.

Friday, June 15, 2012

More on Student Loans

I have been writing (and I use that term loosely) in this blog for about two years now. In that time, our debt has actually increased substantially. To be fair, we had to buy a new car when my old one died a week before Christmas 2010, and we've been hit by flooding in our basement not once, but twice, but mostly we're just irresponsible and spend money that we don't have.

We lack self control. We can't tell ourselves no. Vacations? Sure. Dinner out? Why not! Buy the kids a toy? Absolutely!

The thing is, although we have a ton of debt and make massive payments every month, we don't struggle financially for the most part, so it doesn't seem like it's that big of an issue. Until now. Well, it's still not that big of an issue, but my husband has told me that we can not have another baby (which I want badly) until we move out of this house and pay off our credit card debt. He said if our credit cards were paid off by next year, we could try to get pregnant again next year.

Challenge accepted!

I previously wrote that we were working towards refinancing our mortgage. It will save us $225 a month, once all is said and done. Well, I also decided to consolidate my student loans, as interest rates on my variable loans will be increasing on July 1 and I wanted to lock in my lower interest rates.

I've noticed that MOST random readers come by my blog searching for information on grandfathered repayment plans on student loans, so I thought I'd take this opportunity to write a little more about it.

I'm not sure when the repayment plans updated, however when I attempted to change my repayment plan a few years ago, I received notice that my student loans were in the grandfathered graduated repayment plan and that changing my repayment plan meant I couldn't go back. I wasn't really sure what the difference was between the two repayment plans, so I didn't change anything. Even looking at the two repayment plans now, I do not see a significant difference, except that if I were to choose the new grandfathered repayment plans, my initial payments would be about $40 less a month than what I'm paying now and would eventually reach a dollar more than my highest payment at the end of the repayment period. The payments start at a lower amount and have a higher increase at each step. I've included an image below of what my payments look like under each scenario.

Points to Remember:

1) When I initially consolidated my loans, I was able to consolidate while still in school and maintain my grace period after graduation. I do not believe this is the case anymore.

2) Also, at the time that I took out my loans, all loans were variable rates. I believe they're now fixed rate only. Since I haven't taken out any student loans in the past seven years, I can't guarantee this is the case, but that is my understanding.

3) The only reason I am able to consolidate now is because my first consolidation loan was disbursed in June of 2005. My final quarter of college was summer 2005, and my loans for that quarter were not disbursed until July 2005, so they were not included in my original consolidation loan. If I were to take out more loans to go back to school in the future, I would be able to consolidate again, assuming they were federal loans.

Ultimately, I decided to go with the Standard repayment plan after this consolidation. The loan payment will be a whopping $15 dollars more a month and it will be a fixed payment for the duration of my loan. As you can see from my chart, payments are being stretched out to 20 years again, so my loans are currently scheduled to be paid off a year later than what is currently slated, but once I've paid off my credit cards, I will be able to pay off the student loans faster and hopefully not pay on these loans till 2032 (at which time my daughter will be 26 and my son will be 24).

We lack self control. We can't tell ourselves no. Vacations? Sure. Dinner out? Why not! Buy the kids a toy? Absolutely!

The thing is, although we have a ton of debt and make massive payments every month, we don't struggle financially for the most part, so it doesn't seem like it's that big of an issue. Until now. Well, it's still not that big of an issue, but my husband has told me that we can not have another baby (which I want badly) until we move out of this house and pay off our credit card debt. He said if our credit cards were paid off by next year, we could try to get pregnant again next year.

Challenge accepted!

I previously wrote that we were working towards refinancing our mortgage. It will save us $225 a month, once all is said and done. Well, I also decided to consolidate my student loans, as interest rates on my variable loans will be increasing on July 1 and I wanted to lock in my lower interest rates.

I've noticed that MOST random readers come by my blog searching for information on grandfathered repayment plans on student loans, so I thought I'd take this opportunity to write a little more about it.

I'm not sure when the repayment plans updated, however when I attempted to change my repayment plan a few years ago, I received notice that my student loans were in the grandfathered graduated repayment plan and that changing my repayment plan meant I couldn't go back. I wasn't really sure what the difference was between the two repayment plans, so I didn't change anything. Even looking at the two repayment plans now, I do not see a significant difference, except that if I were to choose the new grandfathered repayment plans, my initial payments would be about $40 less a month than what I'm paying now and would eventually reach a dollar more than my highest payment at the end of the repayment period. The payments start at a lower amount and have a higher increase at each step. I've included an image below of what my payments look like under each scenario.

Points to Remember:

1) When I initially consolidated my loans, I was able to consolidate while still in school and maintain my grace period after graduation. I do not believe this is the case anymore.

2) Also, at the time that I took out my loans, all loans were variable rates. I believe they're now fixed rate only. Since I haven't taken out any student loans in the past seven years, I can't guarantee this is the case, but that is my understanding.

3) The only reason I am able to consolidate now is because my first consolidation loan was disbursed in June of 2005. My final quarter of college was summer 2005, and my loans for that quarter were not disbursed until July 2005, so they were not included in my original consolidation loan. If I were to take out more loans to go back to school in the future, I would be able to consolidate again, assuming they were federal loans.

Ultimately, I decided to go with the Standard repayment plan after this consolidation. The loan payment will be a whopping $15 dollars more a month and it will be a fixed payment for the duration of my loan. As you can see from my chart, payments are being stretched out to 20 years again, so my loans are currently scheduled to be paid off a year later than what is currently slated, but once I've paid off my credit cards, I will be able to pay off the student loans faster and hopefully not pay on these loans till 2032 (at which time my daughter will be 26 and my son will be 24).

On a side note, I was reading this article about Private Student Loans. I find it disturbing that so many people are struggling with student loans, and there really isn't anything that can be done about the private loans. But that is a story for another day.

Wednesday, May 30, 2012

Random Thoughts

I am at work and running a macro on my system right now, so it seems like the perfect opportunity to write a blog entry. Yay!

I originally planned to write about my experiences with my Discover Card. I got the Discover Card in December for a balance transfer at 15 months no interest. I really had no intention of using the card for actual purchases, but then I started looking into their 5% cash back bonus rewards and thought I would try it out for the month of May. From April through June, the card pays 5% cash back on restaurants and movies, and for the month of May, there was an additional cash back bonus of 5% for grocery store purchases. Additionally, they have a promotion through 2012 where you get 2% cash back on telecommunications purchases (phone, internet, cable, satellite radio) that you have automatically paid with your Discover Card.

Now, I know I'm supposed to be watching our spending, but we go out to eat. We usually go out at least once on the weekend, and I go out sometimes during the week - usually on Friday's, but sometimes more often than that. It just depends on what my coworkers do for lunch. Knowing I'd be getting 5% back on each purchase that I made, and knowing that I was going to be making the purchases anyway, made me question why I wasn't taking advantage of this rewards program. I was already using my credit union card for their 1% cash back on most purchases, and it's actually worked out pretty well for me, except that I can't stop spending money.

What I decided to do in May was use my Discover Card for purchases at restaurants and grocery stores (we don't go to the movies), and my credit union card for other purchases. I was guaranteed 5% back on the Discover purchases, and 1% back on the credit union card. The 5% can be redeemed in multiple ways, and the 1% is paid out yearly into a high interest savings account (greater than 10%).

Throughout my first billing cycle (first 27 days of May), I earned more than $15 in rewards, but I'd only made about $60 in purchases at a grocery store.

Now, I should have put more thought into this, but I was trying to act quickly since the transaction had to clear by the end of the month and it was the 28th by time I saw my May statement. I went to my local grocery store with a gas station and bought their gift cards to use for gas and groceries to get the 5% cash back. If I had done more research, I would have realized that the gift cards did not earn me any fuel rewards, however if I had bought cards that earned me fuel rewards, I would not have likely paid more in activation fees than I got back, so it was a toss up. As it is, I earned $10 in cash back and will be able to pay for my gas and groceries with the gift cards. The maximum you can earn this year from the 5% cash back bonus is $315, based on current promtions, plus whatever you earn from regular purchases. My plan is to cash out the cash back rewards at the end of the year to apply towards Christmas. If I redeem my rewards for their partner gift cards, I can increase my rewards and save myself a little more.

Anyway, I planned to write more but it's time to go home. Later.

I originally planned to write about my experiences with my Discover Card. I got the Discover Card in December for a balance transfer at 15 months no interest. I really had no intention of using the card for actual purchases, but then I started looking into their 5% cash back bonus rewards and thought I would try it out for the month of May. From April through June, the card pays 5% cash back on restaurants and movies, and for the month of May, there was an additional cash back bonus of 5% for grocery store purchases. Additionally, they have a promotion through 2012 where you get 2% cash back on telecommunications purchases (phone, internet, cable, satellite radio) that you have automatically paid with your Discover Card.

Now, I know I'm supposed to be watching our spending, but we go out to eat. We usually go out at least once on the weekend, and I go out sometimes during the week - usually on Friday's, but sometimes more often than that. It just depends on what my coworkers do for lunch. Knowing I'd be getting 5% back on each purchase that I made, and knowing that I was going to be making the purchases anyway, made me question why I wasn't taking advantage of this rewards program. I was already using my credit union card for their 1% cash back on most purchases, and it's actually worked out pretty well for me, except that I can't stop spending money.

What I decided to do in May was use my Discover Card for purchases at restaurants and grocery stores (we don't go to the movies), and my credit union card for other purchases. I was guaranteed 5% back on the Discover purchases, and 1% back on the credit union card. The 5% can be redeemed in multiple ways, and the 1% is paid out yearly into a high interest savings account (greater than 10%).

Throughout my first billing cycle (first 27 days of May), I earned more than $15 in rewards, but I'd only made about $60 in purchases at a grocery store.

Now, I should have put more thought into this, but I was trying to act quickly since the transaction had to clear by the end of the month and it was the 28th by time I saw my May statement. I went to my local grocery store with a gas station and bought their gift cards to use for gas and groceries to get the 5% cash back. If I had done more research, I would have realized that the gift cards did not earn me any fuel rewards, however if I had bought cards that earned me fuel rewards, I would not have likely paid more in activation fees than I got back, so it was a toss up. As it is, I earned $10 in cash back and will be able to pay for my gas and groceries with the gift cards. The maximum you can earn this year from the 5% cash back bonus is $315, based on current promtions, plus whatever you earn from regular purchases. My plan is to cash out the cash back rewards at the end of the year to apply towards Christmas. If I redeem my rewards for their partner gift cards, I can increase my rewards and save myself a little more.

Anyway, I planned to write more but it's time to go home. Later.

Wednesday, May 23, 2012

Annoyed

We're in the process of refinancing our house. I'm glad that we are, don't get me wrong, but I'm starting to see what others have complained about as far as the harp refinancing process goes.

I applied at the end of April and received the application the following week. I completed the paperwork and collected their list of documents and returned everything.

This past weekend, I received an envelope from US Bank with a new good faith estimate. It, of course, was more - to the tune of $1056 more. They said instead of a two month deposit towards escrow, I have to deposit five months worth.

Now, today, I received an email from the underwriter saying that I need to send my last two years tax returns. My problems with this are multiple.

One, why was this not included on my initial checklist of required documents? We could have returned them at the same time as everything else. Two, US Bank had us sign authorization forms for them to pull our tax transcripts. The information should be exactly the same on the transcript as on the tax return because, you know, the transcript is created based on the return. Three, they want a signed and dated copy of the return. Who do you know that files tax returns by paper? What is the purpose of a signed and dated return?

And finally, why am I jumping through so many hoops to refinance with my current lender? They know I've paid my mortgage for the past five years; every month, on time, in full. Does it matter what my tax return looks like? Has my financial position impacted my ability to pay my mortgage in this time of financial instability? As all of my neighbors have walked away from their homes, leaving mine completely worthless, have I even been late on a payment? It's not like I'm refinancing to a shorter term loan or that my payments are going up. I meet the requirements for refinancing under HARP, so what is the deal???

If I didn't think it's be a bigger hassle to find another lender, I'd scrap this refi and go elsewhere. I thought this would be the path of least resistance.

I applied at the end of April and received the application the following week. I completed the paperwork and collected their list of documents and returned everything.

This past weekend, I received an envelope from US Bank with a new good faith estimate. It, of course, was more - to the tune of $1056 more. They said instead of a two month deposit towards escrow, I have to deposit five months worth.

Now, today, I received an email from the underwriter saying that I need to send my last two years tax returns. My problems with this are multiple.

One, why was this not included on my initial checklist of required documents? We could have returned them at the same time as everything else. Two, US Bank had us sign authorization forms for them to pull our tax transcripts. The information should be exactly the same on the transcript as on the tax return because, you know, the transcript is created based on the return. Three, they want a signed and dated copy of the return. Who do you know that files tax returns by paper? What is the purpose of a signed and dated return?

And finally, why am I jumping through so many hoops to refinance with my current lender? They know I've paid my mortgage for the past five years; every month, on time, in full. Does it matter what my tax return looks like? Has my financial position impacted my ability to pay my mortgage in this time of financial instability? As all of my neighbors have walked away from their homes, leaving mine completely worthless, have I even been late on a payment? It's not like I'm refinancing to a shorter term loan or that my payments are going up. I meet the requirements for refinancing under HARP, so what is the deal???

If I didn't think it's be a bigger hassle to find another lender, I'd scrap this refi and go elsewhere. I thought this would be the path of least resistance.

Tuesday, May 8, 2012

Another day, Another Dollar

Another day, another dollar. Things are continuing down the same path they have been. We got our refinance paperwork last week and I set to work collecting the paperwork they needed to complete our loan. Of course, last Monday my credit union sent me a message on Facebook telling me that they may be able to help me after all and that somebody would call me within a week. Yesterday was a week and I still haven't heard, so I may give another call today. If our credit union is able to do better than our current lender, then I may scrap our current loan application and eat the application and credit report cost.

I also decided to start using my Discover card for automatic payment of some of our bills. They are offering 2% cash back on automatic payments of Cable, Satellite TV, Phone, Internet, and Satellite Radio with the Discover card. I currently pay these bills manually with another rewards card and then pay them off at the end of each month so that they don't incur interest charges. My other rewards card offers 1% cash back, which is deposited into a high interest savings account, which I haven't touched in the past three years, but I thought that earning double the rewards with my Discover card would be a better financial decision. I can cash those rewards in on gift cards for places that we frequent and do more with my money, so it's a win/win for me.

It amazes me that Discover is quickly becoming my second favorite credit card (behind my credit union rewards card). Discover is the company that sued me for a defaulted credit card back in 2001 and I never thought that they would approve me for another card, as I'd always heard that they blacklist those that have previously defaulted on an account. But here I am, with a $10500 credit limit and using it effectively and to my benefit.

Anyway, it's just more of the same in our financial world. Things are slowly but surely getting better and we are making progress. That is the best we can hope for.

I also decided to start using my Discover card for automatic payment of some of our bills. They are offering 2% cash back on automatic payments of Cable, Satellite TV, Phone, Internet, and Satellite Radio with the Discover card. I currently pay these bills manually with another rewards card and then pay them off at the end of each month so that they don't incur interest charges. My other rewards card offers 1% cash back, which is deposited into a high interest savings account, which I haven't touched in the past three years, but I thought that earning double the rewards with my Discover card would be a better financial decision. I can cash those rewards in on gift cards for places that we frequent and do more with my money, so it's a win/win for me.

It amazes me that Discover is quickly becoming my second favorite credit card (behind my credit union rewards card). Discover is the company that sued me for a defaulted credit card back in 2001 and I never thought that they would approve me for another card, as I'd always heard that they blacklist those that have previously defaulted on an account. But here I am, with a $10500 credit limit and using it effectively and to my benefit.

Anyway, it's just more of the same in our financial world. Things are slowly but surely getting better and we are making progress. That is the best we can hope for.

Monday, April 30, 2012

Refinancing

We received our application and paperwork to refinance our home this weekend. The news was even better than I had expected as they are dropping our PMI from nearly $60 per month to less than $18.

By time all is said and done, with the lower interest rate, lower PMI, and lower taxes, as well as a longer mortgage term, we will be saving about $225 a month, which will initially be applied directly to our credit cards and later will be either saved or applied towards principle. It all depends what is going on with the housing market when that time comes. If we're staying put, we'll need to pay five years off our loan. If we're leaving, we'll be saving towards a 20% downpayment to prevent PMI on the next home.

By time all is said and done, with the lower interest rate, lower PMI, and lower taxes, as well as a longer mortgage term, we will be saving about $225 a month, which will initially be applied directly to our credit cards and later will be either saved or applied towards principle. It all depends what is going on with the housing market when that time comes. If we're staying put, we'll need to pay five years off our loan. If we're leaving, we'll be saving towards a 20% downpayment to prevent PMI on the next home.

Monday, April 23, 2012

A Little Early

I may have celebrated a little too early last week. As it turns out, if you include my 401k loan, I am still over $200,000 in debt. However, I did pay off more than $700 in debt this month, and that includes what we charged for our vacation.

Yay, right!? Okay, so I know we shouldn’t have charged our vacation, but I know that my husband is getting a bonus this month and another in three months, so we’ll be able to pay it off by summer. I know we would be further ahead if we had just not taken a vacation, but we enjoyed ourselves and it was really good for us to get away as a family.

But we have gotten some good news and some “good” news in the past couple of days that may bode well for our financial future as it relates to our house. I called my current mortgage lender about refinancing and found out that I can refinance to 4.5%, as opposed to the current 6.0%. There are about $2400 in fees, including appraisal, credit report, closing costs, etc. This will lower our monthly mortgage payment about $140 a month. Because I currently have PMI on my home, they will not let me reduce my mortgage term from 30 years to 15 or 20 years. I’m not sure of the logic of this, aside from the fact that it keeps me paying PMI longer. It doesn’t matter though, because I’m going to continue paying the same amount towards my mortgage to pay my principle off quicker and ultimately get out of PMI quicker.

The other “good” news, that I put in parenthesis because it’s not really good news, but it’s better than the alternative, is that we received word on our appeal of our property value. They decreased our property value 25% for 2010, and 5% for 2011, so we should be receiving a refund of overpaid property taxes and will be paying less going forward.

The combination of these two items means we will likely see a nearly $200 decrease in our monthly mortgage payment. While we’re still stuck in a home that we hate, the extra money means that we can pay off our debt faster.

And finally, here is our current debt picture.

Yay, right!? Okay, so I know we shouldn’t have charged our vacation, but I know that my husband is getting a bonus this month and another in three months, so we’ll be able to pay it off by summer. I know we would be further ahead if we had just not taken a vacation, but we enjoyed ourselves and it was really good for us to get away as a family.

But we have gotten some good news and some “good” news in the past couple of days that may bode well for our financial future as it relates to our house. I called my current mortgage lender about refinancing and found out that I can refinance to 4.5%, as opposed to the current 6.0%. There are about $2400 in fees, including appraisal, credit report, closing costs, etc. This will lower our monthly mortgage payment about $140 a month. Because I currently have PMI on my home, they will not let me reduce my mortgage term from 30 years to 15 or 20 years. I’m not sure of the logic of this, aside from the fact that it keeps me paying PMI longer. It doesn’t matter though, because I’m going to continue paying the same amount towards my mortgage to pay my principle off quicker and ultimately get out of PMI quicker.

The other “good” news, that I put in parenthesis because it’s not really good news, but it’s better than the alternative, is that we received word on our appeal of our property value. They decreased our property value 25% for 2010, and 5% for 2011, so we should be receiving a refund of overpaid property taxes and will be paying less going forward.

The combination of these two items means we will likely see a nearly $200 decrease in our monthly mortgage payment. While we’re still stuck in a home that we hate, the extra money means that we can pay off our debt faster.

And finally, here is our current debt picture.

Wednesday, April 18, 2012

Milestone!

I input all of the payments we've made this month, as I do after every pay day. I put all of our new balances in, taking into account what we spent on vacation. The only outstanding payment we have for April is my car, but I can estimate the balance based on interest rates and fixed payment amounts.

And then I came to a shocking and exciting realization.

For the first time since I started my debt payoff journey, we owe less than $200,000 in debt!

This months debt total is $199,564.32!

Slow and steady wins the race, right?

In other news, I'm trying to refinance our house. Supposedly, HARP 2.0 eliminated a cap on LTV and appraisals on your home. As I am learning, this is not necessarily so. Since financial institutions have a choice in whether they want to offer HARP refinancing or not, most of them are not willing to provide refinancing through this program. Why should they, I guess, when they're making a profit off of those of us that are locked into high interest rates and haven't walked away from our homes yet.

I tried to refinance through my credit union yesterday, but they enforce a 125% LTV cap on their HARP loans. We're looking at closer to 148% based on Zillow's values. Even if we used the higher assessment we received from the auditors office for tax purposes, we're still at 133% LTV.

I hate that we live in a society where I'm being punished for being responsible and paying my mortgage, unlike the majority of my neighbors. I don't know if our situation would be more bearable if we were paying less on our home, but it would certainly lessen the sting. Every day I ask myself why we're still paying our mortgage when all of our neighbors have walked away and the current owners paid 1/3 of what we did for our home. We're gluttons for punishment, I guess.

We have to make a pretty big repair to our home, to the tune of over $8000, but I don't know where we're going to find the money. In better times, we might have been able to take out a home equity line of credit, but since our equity is negative, there is nothing to take out. It's our sewer line, and it's a ticking time bomb. The walls are cracked and it has started to shift in about 1/4-1/2 of an inch. I know we need to fix it, but I don't know where we'll find the money.

Roto Rooter was pretty shady about the whole thing; they told us in our home that it would be a max $4000 to have the work done, so I took a $4000 loan out of my 401k, only for them to give us a proposal of $8175. When I told him he had quoted us $4000 at our home, he said there was no way he would have quoted that because it was impossible and told me to take out a loan for the other $4000. I told him I took out a loan for the first $4000 and it wasn't even in the ballpark of what we were willing to do for our home at this time.

I applied for a new job too. I'm not sure if I am ready to leave where I am, but the job I applied for pays significantly more, and it's more in line with the career path I'm following. We'll see if I even get an interview, and then I will start making decisions if it's necessary.

Alas, I must get back to work, but I wanted to share my good news.

And then I came to a shocking and exciting realization.

For the first time since I started my debt payoff journey, we owe less than $200,000 in debt!

This months debt total is $199,564.32!

Slow and steady wins the race, right?

In other news, I'm trying to refinance our house. Supposedly, HARP 2.0 eliminated a cap on LTV and appraisals on your home. As I am learning, this is not necessarily so. Since financial institutions have a choice in whether they want to offer HARP refinancing or not, most of them are not willing to provide refinancing through this program. Why should they, I guess, when they're making a profit off of those of us that are locked into high interest rates and haven't walked away from our homes yet.

I tried to refinance through my credit union yesterday, but they enforce a 125% LTV cap on their HARP loans. We're looking at closer to 148% based on Zillow's values. Even if we used the higher assessment we received from the auditors office for tax purposes, we're still at 133% LTV.

I hate that we live in a society where I'm being punished for being responsible and paying my mortgage, unlike the majority of my neighbors. I don't know if our situation would be more bearable if we were paying less on our home, but it would certainly lessen the sting. Every day I ask myself why we're still paying our mortgage when all of our neighbors have walked away and the current owners paid 1/3 of what we did for our home. We're gluttons for punishment, I guess.

We have to make a pretty big repair to our home, to the tune of over $8000, but I don't know where we're going to find the money. In better times, we might have been able to take out a home equity line of credit, but since our equity is negative, there is nothing to take out. It's our sewer line, and it's a ticking time bomb. The walls are cracked and it has started to shift in about 1/4-1/2 of an inch. I know we need to fix it, but I don't know where we'll find the money.

Roto Rooter was pretty shady about the whole thing; they told us in our home that it would be a max $4000 to have the work done, so I took a $4000 loan out of my 401k, only for them to give us a proposal of $8175. When I told him he had quoted us $4000 at our home, he said there was no way he would have quoted that because it was impossible and told me to take out a loan for the other $4000. I told him I took out a loan for the first $4000 and it wasn't even in the ballpark of what we were willing to do for our home at this time.

I applied for a new job too. I'm not sure if I am ready to leave where I am, but the job I applied for pays significantly more, and it's more in line with the career path I'm following. We'll see if I even get an interview, and then I will start making decisions if it's necessary.

Alas, I must get back to work, but I wanted to share my good news.

Saturday, March 3, 2012

Miscalculated

I'm glad I slept on it last night and reran the numbers. It made me realize that I miscalculated; the loan payments were biweekly, not monthly, so we can't afford it, and the savings wouldn't be that substantial anyway. I'm back to the drawing board.

My husband and I had a huge argument about budgeting and finances this evening. It ended with me telling him that I just wanted us to be on the same page when it comes to money, because no matter how much I try to pay off debt, it's not going to happen unless we both are willing to change our spending habits. That has led to me deciding tonight that I need to write out my plan to get us out of debt and to lay it out to him so he knows EXACTLY what my plans are and we can BOTH stick to these plans, instead of spending impulsively.

That said, I need to figure out exactly what my plan is.

My husband and I had a huge argument about budgeting and finances this evening. It ended with me telling him that I just wanted us to be on the same page when it comes to money, because no matter how much I try to pay off debt, it's not going to happen unless we both are willing to change our spending habits. That has led to me deciding tonight that I need to write out my plan to get us out of debt and to lay it out to him so he knows EXACTLY what my plans are and we can BOTH stick to these plans, instead of spending impulsively.

That said, I need to figure out exactly what my plan is.

Friday, March 2, 2012

More Thinking

Tonight I've started thinking that maybe I'll take a loan out of my 401(k) to pay off the consolidation loan and one of my student loans. I'm trying to think through the tax ramifications of paying off a student loan early, and really, all of the ramifications of a 401(k) loan. The loan would not be that much, as I have not saved much for retirement, but it would be enough combined with my savings account and tax return to pay off my consolidation loan (10.49% interest rate) and my student loan (5%). By paying off the two and paying back the 401(k), I would save $70 a month, or $630 between next month and the end of the year. Again, this is money that I could put directly towards other debt. So I'd miss out on about $100 worth of tax deduction, but I'd pay $630 less in interest, so I think it's worth it. I just want to make sure I have my numbers right before I request the 401(k) loan because I'd hate to take out the loan to pay off these debts only to not have enough to pay off the two debts I'm planning to pay off and still be making the same number of loan payments.

I can not believe how much time I spend thinking about money. It is 1:30 on a Saturday morning, and I'm sitting here thinking about how best to pay off my credit card debt. I can not imagine how much of my life I'm going to get back once these debts are paid off. Maybe then I'll start spending all of my spare time thinking about how to save money instead.

I finally filed my tax return, so that's a step in the right direction as far as actually accumulating the money that is needed to pay this debt off. I have got to remember what I feel right now next time I want to take out a boatload of debt. Yeah.

I can not believe how much time I spend thinking about money. It is 1:30 on a Saturday morning, and I'm sitting here thinking about how best to pay off my credit card debt. I can not imagine how much of my life I'm going to get back once these debts are paid off. Maybe then I'll start spending all of my spare time thinking about how to save money instead.

I finally filed my tax return, so that's a step in the right direction as far as actually accumulating the money that is needed to pay this debt off. I have got to remember what I feel right now next time I want to take out a boatload of debt. Yeah.

Wednesday, February 29, 2012

C'mon Get Happy

I am in such a great mood this morning. I would be in a better mood if I hadn't acted without thinking, as far as spending my bonus money, but I am in a pretty good mood.

My original plan was to apply my entire bonus and our entire tax return to our two Best Buy cards so that I would eliminate those two payments. I paid off the smaller of the two cards, and I paid off the two purchases on the other card whose promotional interest rates were about to expire. Even though none of the purchases were accumulating interest, I thought that it would be good to eliminate those two payments so I could apply them to other debt.

I have a credit union credit card that we use for our day to day purchases because it offers cash back, so I didn't want to apply it to that card because we're likely to run it back up next month and the benefit is short lived.

I have a Discover card that I transferred balances to in December, but I didn't want to put the bonus towards that because it pretty much would have defeated the balance transfers for the 0% interest for 15 months.

Our Target credit card was already paid off, our credit card with our other credit union was already paid off, and we're on a fixed payment for my consolidation loan.

Doh! My consolidation loan, the loan with the highest interest rate (10.49%). I should have put my bonus towards the consolidation loan. While the thought of eliminating two credit card balances was appealing, the majority of the purchases did not start accruing interest until 2013. The minimum payments were very minimum ($25 and $31), and they were accruing $0 in interest. Applying my bonus to the consolidation loan would have decreased the balance, decreasing the interest that is accruing on the loan, and would have put me in the position to pay the loan off at some point this year. The money that is currently going towards the loan could have then been applied to the Best Buy balances, and they still would have been paid off before they began accruing interest.

Lesson learned.

I can't get the money back that I've already paid out, however the balance of my bonus, plus our tax return that we will hopefully receive in March, will instead be applied to the consolidation loan. Paying off just over 30% of the balance of the loan will greatly decrease the interest that is accruing and in December, I will use our savings accounts to pay off the balance of the loan. And just like that, we will get $177.68 a month back in our pockets every month. Or more accurately, we will get $177.68 to apply towards the Discover Card. Depending on how my bonus looks in December, I will either use the remainder of our savings account to pay off the Discover Card, or if my bonus is looking amazing, I will pay off the balance of the Discover Card next February when I receive my bonus.

The money that I am currently putting towards the consolidation loan ($177.68) and the Discover Card ($244) each month, will pay off the balance of the Best Buy card before any of the remaining purchases begin accruing interest next year. By next July, all of our credit cards will be paid off, except one, and our consolidation loan will be gone.

And, I am going to resume contributing to my Roth 401(k) next month when my raise goes into effect. I will not be contributing at the level that I wanted to (6%) because realistically, we can't afford to right now, but I will be contributing at 3%, which is something, and when I pay off the bulk of my debt by this time next year, I will be able to increase my contributions.

None of this takes into account any raise or bonus that my husband will receive in the coming year. He receives monthly bonuses based on production and quarterly bonuses based on job safety, as well as an annual bonus based on a combination of both. It has been hit or miss whether he has gotten raises from year to year, because he works for a small company, so I never count on his paycheck going up.

I think we have decided to forgo the expensive vacation this year, in favor of saving for a Disney trip next year. If we go on vacation, it will be significantly less expensive than previous years, an less expensive than we had planned with the Disney vacation.

So yeah, right now I'm feeling pretty okay with where our finances are headed, as long as I can reign in my husband's spending. I've been making strides not to go to the store unless I need something so that I do not spend impulsively. My next goal is to create grocery shopping lists so that I do not wonder the aisles aimlessly looking for something to cook and end up coming home with a car full of snack foods and no real meals to speak of.

To close, here is the picture of our current debt distribution, after paying all bills for February. As you can see, the overall percentage of debt that is attributable to credit cards has increased, as has the overall credit card total. This is as a result of my husband buying video games, etc on an impulse.

My original plan was to apply my entire bonus and our entire tax return to our two Best Buy cards so that I would eliminate those two payments. I paid off the smaller of the two cards, and I paid off the two purchases on the other card whose promotional interest rates were about to expire. Even though none of the purchases were accumulating interest, I thought that it would be good to eliminate those two payments so I could apply them to other debt.

I have a credit union credit card that we use for our day to day purchases because it offers cash back, so I didn't want to apply it to that card because we're likely to run it back up next month and the benefit is short lived.

I have a Discover card that I transferred balances to in December, but I didn't want to put the bonus towards that because it pretty much would have defeated the balance transfers for the 0% interest for 15 months.

Our Target credit card was already paid off, our credit card with our other credit union was already paid off, and we're on a fixed payment for my consolidation loan.

Doh! My consolidation loan, the loan with the highest interest rate (10.49%). I should have put my bonus towards the consolidation loan. While the thought of eliminating two credit card balances was appealing, the majority of the purchases did not start accruing interest until 2013. The minimum payments were very minimum ($25 and $31), and they were accruing $0 in interest. Applying my bonus to the consolidation loan would have decreased the balance, decreasing the interest that is accruing on the loan, and would have put me in the position to pay the loan off at some point this year. The money that is currently going towards the loan could have then been applied to the Best Buy balances, and they still would have been paid off before they began accruing interest.

Lesson learned.

I can't get the money back that I've already paid out, however the balance of my bonus, plus our tax return that we will hopefully receive in March, will instead be applied to the consolidation loan. Paying off just over 30% of the balance of the loan will greatly decrease the interest that is accruing and in December, I will use our savings accounts to pay off the balance of the loan. And just like that, we will get $177.68 a month back in our pockets every month. Or more accurately, we will get $177.68 to apply towards the Discover Card. Depending on how my bonus looks in December, I will either use the remainder of our savings account to pay off the Discover Card, or if my bonus is looking amazing, I will pay off the balance of the Discover Card next February when I receive my bonus.

The money that I am currently putting towards the consolidation loan ($177.68) and the Discover Card ($244) each month, will pay off the balance of the Best Buy card before any of the remaining purchases begin accruing interest next year. By next July, all of our credit cards will be paid off, except one, and our consolidation loan will be gone.

And, I am going to resume contributing to my Roth 401(k) next month when my raise goes into effect. I will not be contributing at the level that I wanted to (6%) because realistically, we can't afford to right now, but I will be contributing at 3%, which is something, and when I pay off the bulk of my debt by this time next year, I will be able to increase my contributions.

None of this takes into account any raise or bonus that my husband will receive in the coming year. He receives monthly bonuses based on production and quarterly bonuses based on job safety, as well as an annual bonus based on a combination of both. It has been hit or miss whether he has gotten raises from year to year, because he works for a small company, so I never count on his paycheck going up.

I think we have decided to forgo the expensive vacation this year, in favor of saving for a Disney trip next year. If we go on vacation, it will be significantly less expensive than previous years, an less expensive than we had planned with the Disney vacation.

So yeah, right now I'm feeling pretty okay with where our finances are headed, as long as I can reign in my husband's spending. I've been making strides not to go to the store unless I need something so that I do not spend impulsively. My next goal is to create grocery shopping lists so that I do not wonder the aisles aimlessly looking for something to cook and end up coming home with a car full of snack foods and no real meals to speak of.

To close, here is the picture of our current debt distribution, after paying all bills for February. As you can see, the overall percentage of debt that is attributable to credit cards has increased, as has the overall credit card total. This is as a result of my husband buying video games, etc on an impulse.

Sunday, February 26, 2012

Hello Bonus, Goodbye Bonus

I received my bonus in my paycheck this past week. It ended up being close to $5000, but after they took out taxes, it was less than I expected so I wasn't able to pay off as much as I thought I'd be able to. What I was able to pay off is one of our Best Buy cards, our Target card, and I will be paying off all of the purchases that will begin accumulating interest in the coming months from our other Best Buy card. There will be some money leftover, but I'm not sure if I want to put it towards the Best Buy card, or towards one of my interest accruing accounts. I'm waiting to see how much money we have left in the account once everything I paid has cleared the bank.

One of the other major steps that we finally took was buying additional life insurance. Well, we haven't technically bought it, but once I contact my insurance agent on Monday to make the first two months payment, we will have enough life insurance to pay off our debt if something were to happen to either of us, plus a few years of income. My husband actually qualified for preferred rates, since he quit smoking nearly two years ago. It's going to cost us less than $50 a month, and it's a 20 year term policy. We have until 15 years into the policy to convert them to whole life policies based on our current health.

I also had my year end review this past week and found out that I'm getting a raise the first pay of April. My raise ended up being 3.41%, and my manager told me that was the highest raise that the system would let her give me based on the fact that I got a raise last fall. I have been looking at other jobs, just to see what's out there. While I love the people I work with, I'm not sure that I'm comfortable with the direction my current role is headed, and I know that there are positions available that will pay more and may be better suited for me. I'm trying to decide if I want to stay put and start working on my MBA, or if I want to find another job and work towards my MBA. I'm conflicted because we have such a great team and I think it would be hard to find that same chemistry somewhere else.

I'm trying to figure out how to better use this blog than just documenting how much debt we have every month. It doesn't make for very interesting reading when I only update once a month.

Anyway, I will update with February totals once all of my payments process. Until next time.

One of the other major steps that we finally took was buying additional life insurance. Well, we haven't technically bought it, but once I contact my insurance agent on Monday to make the first two months payment, we will have enough life insurance to pay off our debt if something were to happen to either of us, plus a few years of income. My husband actually qualified for preferred rates, since he quit smoking nearly two years ago. It's going to cost us less than $50 a month, and it's a 20 year term policy. We have until 15 years into the policy to convert them to whole life policies based on our current health.

I also had my year end review this past week and found out that I'm getting a raise the first pay of April. My raise ended up being 3.41%, and my manager told me that was the highest raise that the system would let her give me based on the fact that I got a raise last fall. I have been looking at other jobs, just to see what's out there. While I love the people I work with, I'm not sure that I'm comfortable with the direction my current role is headed, and I know that there are positions available that will pay more and may be better suited for me. I'm trying to decide if I want to stay put and start working on my MBA, or if I want to find another job and work towards my MBA. I'm conflicted because we have such a great team and I think it would be hard to find that same chemistry somewhere else.

I'm trying to figure out how to better use this blog than just documenting how much debt we have every month. It doesn't make for very interesting reading when I only update once a month.

Anyway, I will update with February totals once all of my payments process. Until next time.

Monday, January 9, 2012

I'm So Excited!

Our bonus for 2011 was just updated with November results; December results should be in next week. I am ridiculously excited to see that our bonus this year is projected to be over $4700. This is, far and away, the largest bonus I have ever seen with this company. Generally they just touch $1500, or less. I think I've only gotten over $1000 twice.

Can I just tell you how ridiculously excited I am?! I know they take about 40% of it in taxes, but it will still be enough to pay off both of our Best Buy cards and a portion of one of my interest bearing cards, or my consolidation loan, or something.

I hope there isn't a major letdown with December results.

Ok, you may carry on with your daily lives. I just wanted to express my excitement and didn't want to do so anywhere that may be construed as braggin.

Can I just tell you how ridiculously excited I am?! I know they take about 40% of it in taxes, but it will still be enough to pay off both of our Best Buy cards and a portion of one of my interest bearing cards, or my consolidation loan, or something.

I hope there isn't a major letdown with December results.

Ok, you may carry on with your daily lives. I just wanted to express my excitement and didn't want to do so anywhere that may be construed as braggin.

Sunday, January 1, 2012

Hello 2012

I have told my husband repeatedly, 2012 is the year we pay off our credit card debt. We might not be able to pay off the student loans, cars, house, or signature loan, but in 2012, we are going to pay off our credit cards.

I have started taking some steps to pay them off. I opened a Discover Card and transferred some of my balances to it at 0% interest for 18 months. They each came with a 3% balance transfer fee, but the balance transfer fee on each equals one months interest, so I'm still not going to end up paying as much on the debt. After transferring as much of the balances as I could (I was not able to transfer them all because the credit line was not high enough), I drained our savings accounts so I can pay off the remaining balances on a couple of the cards. We will still have a pretty significant amount of debt accruing interest, but I'm trying to position us so that we can pay it off this year.

I was not 100% what the balances were on the credit cards as I set up the balance transfers so what I did was this:

Estimated that our Target card had a balance of about $3500, but was not sure of the exact amount, so I transferred $3000 to the Discover card and used a portion of our savings to pay the remaining balance.

One of our Credit Union cards had a balance of about $2100, but I wasn't sure of the exact amount, so I transferred $2100 and used savings to pay the remaining balance.

I used savings to pay off our Kohl's card and my Victoria's Secret credit card.

My husband's paycheck should be pretty big next week, since he worked the full week, plus got paid for an extra day for Christmas and for New Years, so 20 hours extra on top of the full two weeks worth of work, plus he'll be receiving a bonus (possibly two, depending how long it takes for them to pay the second). My bonus will come in February and it is pretty sizable this year.

I think between the two, we should be able to pay off all of our credit card debt that is currently accruing interest. We will have a Discover Card and two Best Buy cards that have debt that are accruing 0% interest, which we should be able too pay off throughout the year and should be, hopefully, credit card debt free by the end of 2012.

The biggest challenge for us is that we don't want to stop spending. We have real issues controlling our spending. Even as we've had the conversations as they've related to what we need to do to pay off the debt, we're still talking about taking a Disney vacation, which would have to be charged, and we still make random trips to the store whenever we're bored and just buy whatever. We still can't exhibit the will power we need to be successful in this resolution, so that may take a lot more time and effort than even I expect.