This is going to sound horrible to say, especially in today’s economy.

My job is so boring. I should be glad; it gives me plenty of time to search the internet for interesting articles. I can do a lot of research on how to save money, how to spend money, and how to live more frugally. My actual work load encompasses about five days a month, and then for the rest of the month, I’m left wondering what I’m supposed to do. Maybe I just work faster than others? Other people doing the same job make it sound like they have no time and have to put in extra house. I’m more inclined to believe that they spend just as much time surfing the internet as I do; they just don’t feel bad about it. But, I’m glad I have a job in this economic climate, so I’ll keep doing my thing with the illusion of being busy.

Today I found two different articles that I found interesting (and it’s only 11:00!). The first is What You Should Expect from Social Security. I don’t have much to say on it, just found it interesting. I’ve become particularly interested in how I’m going to fund my retirement as of late, although I’m only 29 years old, because I hear so much dire information regarding the future. Last week I read an article about how the government is going to confiscate private pensions and 401(k)’s and redistribute the wealth. All of the comments on it were paranoia inducing. People were talking about withdrawing their entire 401(k) and hiding it under a mattress, stocking up on guns and non-perishable items because “the revolution is coming.” I don’t really believe that is going to happen, but I do think it is going to get worse before it gets better. I would still like to contribute to my 401(k) because my company matches 50 cents on the dollar up to 6% of my pay. It’s a 50% return on my investment just by investing. I will never contribute more than 6% of my pay though, because I see no benefit to it. I would rather put additional funds in an IRA, a savings account, CD’s, money market…. Somewhere that I have a little more access to if I need it. I contribute to a Roth, so I’m not getting the tax savings that are touted by professionals. I would like to know how to do things myself, like sewing, knitting, growing a garden, etc, because if there ever is some sort of total economic breakdown, I would like to have some skill that would be beneficial to my family and would provide a product that could be traded/bartered. Doomsday scenario, but I like to be prepared.

Anyway, enough on that. The second article I read was 6 Ways to Save $2997 a year on Food. I didn’t find the article itself very useful, but the comments were rather interesting. I do not follow an across the board “eating out is more expensive than eating in” mentality. We have started eating in more, with me cooking more dinners and we have been buying less fast food since we started buckling down. We still eat out on occasion, but we were eating out three to four nights a week, every weekday morning for breakfast, and every weekday afternoon for lunch.

I have not stuck so steadfastly to my “I’m not eating out anymore” because we haven’t been to the grocery store for a real shopping trip in probably a month. We’ve stopped here and there to buy little things but for the most part, no grocery shopping. We’ve tried to decrease our grocery bill, along with our fast food bill, and I think it has been largely successful.

Below are the common philosophies that I use when preparing meals. They change often, but these are pretty constant.

1. Plan meals ahead, but don’t assume that you have to put all of the ingredients in them. For example, a lot of the recipes that I use have a lot of very specific spices, some that I can’t find, some that are just way too expensive for a single meal, so I adjust the recipe to fit our budget and it still comes out delicious.

2. Sometimes, eating out is less expensive than eating in, even if it isn’t healthy. We stop at Little Caesars every couple of weeks when I don’t feel like cooking. One large one topping pizza costs us $5 and feeds the whole family. A $5 footlong sub is less expensive than buying 3 different kinds of lunch meat, bread, condiments, and veggies.

3. One of the most delicious meals that I make is a whole fryer chicken that I cook in the oven, and it’s pretty cost effective as well. I buy a whole fryer ($0.79/lbs- usually $4.50 for the bird), a garlic bulb ($3.69/lbs- usually about $0.39 for the bulb), celery, baby carrots, an onion, and some red potatoes. Last time, I soaked the chicken overnight in a brine mixture of kosher salt and water, and patted it dry, rubbed the outside of the chicken with a tbsp of butter, then combined spices; salt (I prefer kosher), pepper (fresh ground for me), garlic powder, onion powder, parsley, thyme, whatever I feel like throwing in. I rub it all over the inside and outside of the chicken, and put some between the skin and the meat. I crack a couple of cloves of garlic away from the skin and put those, along with some onion, in the bird. The bird then goes in my roasting pan, and I put a combination of the other veggies into the bottom of the pan. Last time I made it, I poured ¼ cup of white wine over the vegetables (we got the wine at cost, because my husband works for a wine distributor), and then roasted it in the oven at about 400 degrees for an hour, until the juices run clear.

For one thing, it’s really, really good. The meat is usually juicy and tender, and very flavorful. It also provides a lot of meat. The kids like it, I take leftovers for lunch the next day, and sometimes for two days, so for less than ten dollars, we’ve gotten three meals, one of which feeds four people.

I have a lot of favorite “go to” recipes. Maybe one of these days I’ll get around to posting them all, or I can post one a day or something.

5. I know some people baulk at the idea of packing a lunch, however I’ve found that it saves a lot of money; probably $400-$500 a month for me alone. Usually I take a $2 frozen meal, but I do enjoy the nights that I have leftovers for lunch. Dinners like spaghetti, where we usually have a lot of extra, can provide up to three days worth of meals.

6. If there is a local meet shop, mom and pop grocery store, ethnic food store, or whatever, check it out for specials. A few weeks ago, I went into Carfagna’s. They had 15-20 lbs New York Striploin for $2.99/lbs, which they would cut into steaks for you—free of charge. We got a 20 lbs striploin, which generated 20 steaks and 2.5 lbs of ground sirloin for about $60. Even if it were just the steaks, we would have been spending about $3 per steak, which is a phenomenal deal, but the ground sirloin was so much more flavorful than anything we pick up in the grocery store. They also have great prices on fresh produce and a wide variety of cheeses that I don’t find anywhere else.

Anyway, the stuff I do is pretty basic, but it amazed me to read on that article that people don’t think cooking in or taking lunches makes a huge difference to your bottom line or is more expensive. I used to think so too, until I really added up how much we were spending on fast food.

Thursday, October 28, 2010

Wednesday, October 27, 2010

Day 137: Self Pity

It’s time to face the facts; I can’t stop spending. I keep making all of these grand plans about how we’re going to pay off our debt, but neither my husband nor I are willing to make the changes necessary to actually follow through. I obsess daily about how we’re going to pay the debt off in this time frame, making this amount of payments, contributing this amount of bonuses towards debt pay off, and tax returns, and whatever additional windfalls we come across, but the simple fact is that we never follow through.

This week, I have added to my Target card, twice. We went to dinner last Friday and spent $40, then went to Target and spent another $65. Some of it was necessities, most of it was not. The problem is, by time I pay our mortgage, utilities, insurance, car, student loans, and credit cards; we have no money for anything else. We don’t have money to go grocery shopping, or for gas, or to buy clothes that the kids need for winter, so they go on the credit cards, which means the minimum payments never drop and neither do the balances. Instead, we stay in this same never ending cycle where we’re just throwing money down a rabbit hole.

Today I feel dejected, and I feel like a failure. How long have I been at this? And how much progress have I made? My brake light popped on this morning while driving to work. I remember how much it cost to replace my brakes last time. There is always something that comes up. It’s great that we’re getting $1400 back from the county, but when half of that goes towards new brakes… it doesn’t really leave much for credit cards and savings. There’s always something.

This week, I have added to my Target card, twice. We went to dinner last Friday and spent $40, then went to Target and spent another $65. Some of it was necessities, most of it was not. The problem is, by time I pay our mortgage, utilities, insurance, car, student loans, and credit cards; we have no money for anything else. We don’t have money to go grocery shopping, or for gas, or to buy clothes that the kids need for winter, so they go on the credit cards, which means the minimum payments never drop and neither do the balances. Instead, we stay in this same never ending cycle where we’re just throwing money down a rabbit hole.

Today I feel dejected, and I feel like a failure. How long have I been at this? And how much progress have I made? My brake light popped on this morning while driving to work. I remember how much it cost to replace my brakes last time. There is always something that comes up. It’s great that we’re getting $1400 back from the county, but when half of that goes towards new brakes… it doesn’t really leave much for credit cards and savings. There’s always something.

Tuesday, October 19, 2010

Day 129: Rambling about the Past and the Future

I read this article on Yahoo yesterday, regarding 401(k) matching. As I wrote about a month or so ago, I discontinued my 401(k) contributions temporarily because we needed the additional income to help pay our bills and I was facing a consistent negative rate of return on my investment.

Reading the comments on this article (which is no small feat, given the numerous server errors that plague Yahoo articles), made me really think about my investment philosophy and planning for our future retirement.

I don’t know if I’ve spilled any personal information about myself, but I am 29 years old and my husband is in his mid-30s. I make approximately $42,000 a year plus bonuses (which have ranged anywhere from $500 up to an anticipated bonus this year of closer to $1500). My husband is on an hourly wage and generally has a gross income between $21,000-$25,000 and has not seen a raise in three years. Given our yearly salaries, I find it very sad that we have no savings accounts to speak of.

I put $25 per paycheck into each of our children’s savings accounts and then transfer those funds into small, short term CD’s whenever the savings account balances reach $500. I keep the CD’s small, and occasionally have multiple CD’s with different maturity dates, usually only buying 3 month CD’s due to the low savings rate. If the savings rate ever increases (which I anticipate it will in the future), I may buy more long term CD’s. My children know these bank accounts exist, even if they don’t fully understand them. In addition to my automatic contributions every two weeks, we also put any change and cash they receive into their piggy banks, and when the piggy banks get full, we take the piggy’s to the bank, dump the change into the change machine, and deposit that money into their savings accounts as well. When they get older, I will teach them how money is used to buy things, and we will maybe put half of their change into savings, and the rest of it will be used to buy things they want. I will also give them an allowance for doing chores around the house; something I never received growing up.

I think a lot of my financial immaturity can be traced back to my parents and how I was raised. I don’t want to blame my parents, because they did the best they could, given their financial position. They were both teenagers when I was born and my mom dropped out of school at 16. My dad graduated, but always worked hard, manual labor jobs just to make ends meet. They had five kids, and then divorced, and spent the next 14 years arguing over money, child support, medical bills, and everything else. I remember my dad, over and over again, telling me and my siblings how my mom was being unreasonable, expecting him to pay half of the medical and dental bills when he already paid child support, even though that was what the court order stated. I remember him showing me his paychecks and telling me, “This is how much I bring home, and this is how much I pay your mom, and how much does that leave me with? Do you think that it’s fair that I should have to pay her more for doctors and dentist bills?” Similarly, I remember copying every check that my dad sent my mom for child support so she would have proof for the courts that he wasn’t paying his fair share, and knowing how much she was bringing in, and how much the mortgage was, and really having no clue on utilities or car payments. Based on what I know now, as an adult, it’s no wonder our home was foreclosed on when I was 17 years old.

When we bought our house, we made an effort to determine how much home we could afford. I never wanted my children to feel the sense of loss that I did when we lost our home. It was as if I went off to college, and never had a home to go back to. Apartments never felt like home, and I moved every year so I didn’t really accumulate much from year to year. My first apartment was furnished, but my second was not, and the only furniture I owned was a queen sized bed and a 19” tv. I sat the tv on a box and didn’t have cable. My living room was empty. Same with my second apartment, until my (now) husband bought me a tv stand to set my tv on for my birthday. It wasn’t until I moved in with my husband that I actually had furniture in my living room, and even then we had a broken down couch that he’d gotten from friends, or family, or somewhere, and a dresser that had broken handles. We got a free washer and dryer when we signed a 15 month lease with the apartment complex, which worked great for us at the time. We got an old desk from a friend that was moving and furniture from friends and family when they replaced theirs.

So as we were saving to buy a house, we calculated how much we were spending on rent, and we put whatever we could into savings every month. We kept track of what we were able to save, what we were spending on extraneous items, and where we could save more. When we met with a mortgage broker, we told him we could afford no more than $950 a month for our mortgage, interest, and insurance; knowing that we could afford closer to $1000, but not wanting to push our budget. He told us that with the amount we were looking to spend, we could only afford a $100,000 house, but that with our income, we qualified for $160,000 home. We disagreed, telling him that $1000 would be pushing our budget and he told us that we would see raises and be able to afford more in the future. I am glad we didn’t listen to him.

We looked at homes between $99,000 and $113,000, and ultimately bought the most expensive one that we looked at, but it had four bedrooms and one and a half baths, and did not need near the work that the others we saw needed. It was, for all intents and purposes, move in ready.

When we bought our home is when finances started going downhill for us. We bought a new couch, new bed, new tv, new tv stands. It was almost as if when we were told we could afford more house, we thought we could afford more stuff to go in it. Of course, we had no more cash, and since our mortgage payment was at the top of our limit, everything went on credit. At a time when many people were losing their job and defaulting on debt payments, we were a great asset to companies looking to make a profit, like banks. We bought and bought and made the minimum payments and finally, at Christmas last year, hit a point where we were questioning how we were going to buy gifts for everybody that we were supposed to buy for. We had been buying with the assumption that our tax return would bail us out, that bonuses would hold us over, that all of the spending that we did throughout the year would be wiped out with the influx of cash in the spring.

The problem was that with the credit card reform that went into effect earlier this year, some of our creditors, especially the ones with the biggest balances, decided to change their fixed rate cards into variable rates, and increased the interest rates to the point that 90%+ of our minimum payment was going towards interest. This led to higher minimum payments to cover the interest plus a minimum payment towards the balance, and without the tax return, we didn’t have the money to pay the balances down.

Then we were hit by problem after problem financially. Our air conditioner broke, twice. Our basement flooded with sewage. Our air conditioner broke again. The bottom of our car was rusted out and it would have cost more to repair than it was worth to keep it.

Through it all, though, we’ve managed to keep our heads above water. Our 2010 tax return went towards paying off the credit cards we used to fix our basement. Our 2011 tax return will go towards the other problems we’ve had crop up throughout the year.

Once we’ve made a sizable dent in our debt, I will start putting a percentage of our pay into savings for a rainy day fund, instead of throwing so much money towards the debt, that way we will have a cushion. We’re less stressed with an emergency fund.

And after we’ve made payments towards these credit cards and I feel that we have sufficiently gotten our heads above water, I will resume contributions to my company 401(k). My company matches 50 cents on the dollar up to 6% of my salary. I contribute to a Roth 401(k) because I’d like to think that I will be making more money when I retire than I do now, pushing me into a higher tax bracket. Even if I’m not making anymore, I will still probably be in a higher tax bracket due to inflation. After contributing to the maximum that my employer will match, I plan to contribute to a Roth IRA, eventually up to the maximum that I am allowed. I would eventually like to put some amount into the market for long term investing, not to play the market. I want to learn more about buying stock and diversifying my investments. My company also offers a pension, in addition to the 401(k), which I am well aware makes me very fortunate.

Anyway, this discussion about planning for retirement has gotten very long winded and off track, but I guess I just needed a brain dump today. To sum it up, I want to diversify. I know that 401(k)’s aren’t guaranteed, so I’d like to also contribute to a Roth IRA and savings and CD’s, but I’d also like to try some long term investing in the stock market, and hopefully by time we retire, we’ll have paid off our mortgage and won’t be carrying debt, and we’ll be able to live comfortably without worrying where our next meal is coming from.

Reading the comments on this article (which is no small feat, given the numerous server errors that plague Yahoo articles), made me really think about my investment philosophy and planning for our future retirement.

I don’t know if I’ve spilled any personal information about myself, but I am 29 years old and my husband is in his mid-30s. I make approximately $42,000 a year plus bonuses (which have ranged anywhere from $500 up to an anticipated bonus this year of closer to $1500). My husband is on an hourly wage and generally has a gross income between $21,000-$25,000 and has not seen a raise in three years. Given our yearly salaries, I find it very sad that we have no savings accounts to speak of.

I put $25 per paycheck into each of our children’s savings accounts and then transfer those funds into small, short term CD’s whenever the savings account balances reach $500. I keep the CD’s small, and occasionally have multiple CD’s with different maturity dates, usually only buying 3 month CD’s due to the low savings rate. If the savings rate ever increases (which I anticipate it will in the future), I may buy more long term CD’s. My children know these bank accounts exist, even if they don’t fully understand them. In addition to my automatic contributions every two weeks, we also put any change and cash they receive into their piggy banks, and when the piggy banks get full, we take the piggy’s to the bank, dump the change into the change machine, and deposit that money into their savings accounts as well. When they get older, I will teach them how money is used to buy things, and we will maybe put half of their change into savings, and the rest of it will be used to buy things they want. I will also give them an allowance for doing chores around the house; something I never received growing up.

I think a lot of my financial immaturity can be traced back to my parents and how I was raised. I don’t want to blame my parents, because they did the best they could, given their financial position. They were both teenagers when I was born and my mom dropped out of school at 16. My dad graduated, but always worked hard, manual labor jobs just to make ends meet. They had five kids, and then divorced, and spent the next 14 years arguing over money, child support, medical bills, and everything else. I remember my dad, over and over again, telling me and my siblings how my mom was being unreasonable, expecting him to pay half of the medical and dental bills when he already paid child support, even though that was what the court order stated. I remember him showing me his paychecks and telling me, “This is how much I bring home, and this is how much I pay your mom, and how much does that leave me with? Do you think that it’s fair that I should have to pay her more for doctors and dentist bills?” Similarly, I remember copying every check that my dad sent my mom for child support so she would have proof for the courts that he wasn’t paying his fair share, and knowing how much she was bringing in, and how much the mortgage was, and really having no clue on utilities or car payments. Based on what I know now, as an adult, it’s no wonder our home was foreclosed on when I was 17 years old.

When we bought our house, we made an effort to determine how much home we could afford. I never wanted my children to feel the sense of loss that I did when we lost our home. It was as if I went off to college, and never had a home to go back to. Apartments never felt like home, and I moved every year so I didn’t really accumulate much from year to year. My first apartment was furnished, but my second was not, and the only furniture I owned was a queen sized bed and a 19” tv. I sat the tv on a box and didn’t have cable. My living room was empty. Same with my second apartment, until my (now) husband bought me a tv stand to set my tv on for my birthday. It wasn’t until I moved in with my husband that I actually had furniture in my living room, and even then we had a broken down couch that he’d gotten from friends, or family, or somewhere, and a dresser that had broken handles. We got a free washer and dryer when we signed a 15 month lease with the apartment complex, which worked great for us at the time. We got an old desk from a friend that was moving and furniture from friends and family when they replaced theirs.

So as we were saving to buy a house, we calculated how much we were spending on rent, and we put whatever we could into savings every month. We kept track of what we were able to save, what we were spending on extraneous items, and where we could save more. When we met with a mortgage broker, we told him we could afford no more than $950 a month for our mortgage, interest, and insurance; knowing that we could afford closer to $1000, but not wanting to push our budget. He told us that with the amount we were looking to spend, we could only afford a $100,000 house, but that with our income, we qualified for $160,000 home. We disagreed, telling him that $1000 would be pushing our budget and he told us that we would see raises and be able to afford more in the future. I am glad we didn’t listen to him.

We looked at homes between $99,000 and $113,000, and ultimately bought the most expensive one that we looked at, but it had four bedrooms and one and a half baths, and did not need near the work that the others we saw needed. It was, for all intents and purposes, move in ready.

When we bought our home is when finances started going downhill for us. We bought a new couch, new bed, new tv, new tv stands. It was almost as if when we were told we could afford more house, we thought we could afford more stuff to go in it. Of course, we had no more cash, and since our mortgage payment was at the top of our limit, everything went on credit. At a time when many people were losing their job and defaulting on debt payments, we were a great asset to companies looking to make a profit, like banks. We bought and bought and made the minimum payments and finally, at Christmas last year, hit a point where we were questioning how we were going to buy gifts for everybody that we were supposed to buy for. We had been buying with the assumption that our tax return would bail us out, that bonuses would hold us over, that all of the spending that we did throughout the year would be wiped out with the influx of cash in the spring.

The problem was that with the credit card reform that went into effect earlier this year, some of our creditors, especially the ones with the biggest balances, decided to change their fixed rate cards into variable rates, and increased the interest rates to the point that 90%+ of our minimum payment was going towards interest. This led to higher minimum payments to cover the interest plus a minimum payment towards the balance, and without the tax return, we didn’t have the money to pay the balances down.

Then we were hit by problem after problem financially. Our air conditioner broke, twice. Our basement flooded with sewage. Our air conditioner broke again. The bottom of our car was rusted out and it would have cost more to repair than it was worth to keep it.

Through it all, though, we’ve managed to keep our heads above water. Our 2010 tax return went towards paying off the credit cards we used to fix our basement. Our 2011 tax return will go towards the other problems we’ve had crop up throughout the year.

Once we’ve made a sizable dent in our debt, I will start putting a percentage of our pay into savings for a rainy day fund, instead of throwing so much money towards the debt, that way we will have a cushion. We’re less stressed with an emergency fund.

And after we’ve made payments towards these credit cards and I feel that we have sufficiently gotten our heads above water, I will resume contributions to my company 401(k). My company matches 50 cents on the dollar up to 6% of my salary. I contribute to a Roth 401(k) because I’d like to think that I will be making more money when I retire than I do now, pushing me into a higher tax bracket. Even if I’m not making anymore, I will still probably be in a higher tax bracket due to inflation. After contributing to the maximum that my employer will match, I plan to contribute to a Roth IRA, eventually up to the maximum that I am allowed. I would eventually like to put some amount into the market for long term investing, not to play the market. I want to learn more about buying stock and diversifying my investments. My company also offers a pension, in addition to the 401(k), which I am well aware makes me very fortunate.

Anyway, this discussion about planning for retirement has gotten very long winded and off track, but I guess I just needed a brain dump today. To sum it up, I want to diversify. I know that 401(k)’s aren’t guaranteed, so I’d like to also contribute to a Roth IRA and savings and CD’s, but I’d also like to try some long term investing in the stock market, and hopefully by time we retire, we’ll have paid off our mortgage and won’t be carrying debt, and we’ll be able to live comfortably without worrying where our next meal is coming from.

Monday, October 18, 2010

Day 128: Tiptoeing Forward

We’ve had a small step forward this month; or maybe a big step, depending on how you want to define it. Our debt actually went down across all categories, even credit cards. Only one credit card balances actually went up, but everything else was down. All told, we cut over $888 from our debt balance. It is a very exciting month for me, and the fact that my husband finally seems to be getting on board with some of my plans makes me very excited for us as a family and our financial picture.

We also got some good news from the county last week. They will be reimbursing us the out of pocket expenses that we incurred in January as a result of the county’s sanitary sewer flooding our basement. We will be receiving $1377 back from the county. My husband and I have discussed it and decided that $377 of that will be going towards credit card balances, and the other $1000 will go into a savings account for an emergency fund. We debated putting the entire amount towards a credit card, but decided that we are less stressed when we have an emergency cushion, even if it is only $1000.

We will be paying our Target credit card off in the spring, when we receive our tax return. Knowing that we give the government a “loan” every year doesn’t feel so bad when I know we’re getting a chunk back to apply towards our credit cards. I’ve already sat down and planned out where the money is going to go based on the expected refund. Last year we received a refund of over $4000. This year I anticipate it will be closer to $3000 because I’ve recently adjusted my withholding to put more money towards debt now, instead of waiting until tax time. I have abandoned my plan of paying off both Best Buy credit cards with the tax return because we’re not paying interest on them and I felt It was more important to pay the cards that we are paying interest on off.

I can’t wait to watch balances turn to $0. In March, the Target will be at $0, then in June, Best Buy #1 will be at $0, and then December will be Best Buy #2. With my anticipated bonus in April, we may even be able to pay down half the balance on CU 1 in the spring. The thought of eliminating that much debt makes me so giddy. More than that, the thought of being able to save money, instead of putting it all towards debt, makes me giddy.

We have been doing better than I anticipated at paying off debt and staying within our means. I may be able to resume contributions to my 401(k) after the first of the year. I just feel good.

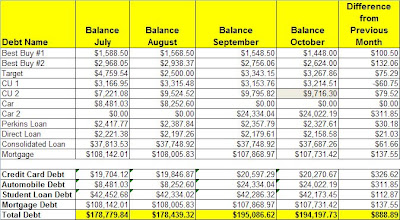

Here is a picture of where the debt is as of the time that all October payments are made. The total for CU 2 is in gray because it has not yet been paid, but this is an estimate based on the minimum payment and total amount that will be applied towards interest.

We also got some good news from the county last week. They will be reimbursing us the out of pocket expenses that we incurred in January as a result of the county’s sanitary sewer flooding our basement. We will be receiving $1377 back from the county. My husband and I have discussed it and decided that $377 of that will be going towards credit card balances, and the other $1000 will go into a savings account for an emergency fund. We debated putting the entire amount towards a credit card, but decided that we are less stressed when we have an emergency cushion, even if it is only $1000.

We will be paying our Target credit card off in the spring, when we receive our tax return. Knowing that we give the government a “loan” every year doesn’t feel so bad when I know we’re getting a chunk back to apply towards our credit cards. I’ve already sat down and planned out where the money is going to go based on the expected refund. Last year we received a refund of over $4000. This year I anticipate it will be closer to $3000 because I’ve recently adjusted my withholding to put more money towards debt now, instead of waiting until tax time. I have abandoned my plan of paying off both Best Buy credit cards with the tax return because we’re not paying interest on them and I felt It was more important to pay the cards that we are paying interest on off.

I can’t wait to watch balances turn to $0. In March, the Target will be at $0, then in June, Best Buy #1 will be at $0, and then December will be Best Buy #2. With my anticipated bonus in April, we may even be able to pay down half the balance on CU 1 in the spring. The thought of eliminating that much debt makes me so giddy. More than that, the thought of being able to save money, instead of putting it all towards debt, makes me giddy.

We have been doing better than I anticipated at paying off debt and staying within our means. I may be able to resume contributions to my 401(k) after the first of the year. I just feel good.

Here is a picture of where the debt is as of the time that all October payments are made. The total for CU 2 is in gray because it has not yet been paid, but this is an estimate based on the minimum payment and total amount that will be applied towards interest.

Monday, October 11, 2010

Day 121: Little Failures

I haven’t had much to write, and I haven’t really wanted to reflect on my failures this month. Everything went up except for the two categories that could only go down. Credit card balances are up, we have our new car loan, and we’re pushing closer to $200,000 in debt than we ever have been before. Even though the balances on both of our Best Buy cards are going down, pretty much every other card has gone up.

My husband and I have been arguing about what exactly a budget it. He doesn’t seem to grasp the concept. He thinks that you can’t budget because “little things pop up” and I’ve told him repeatedly that the point of a budget is that those little things don’t pop up. He’s not talking about emergencies; he’s talking about wanting to go out on weekly shopping trips for non-necessities, like books, like clothes, like toys. As long as he thinks that a budget is supposed to be busted by these “little things that pop up” we will never get on track financially, no matter how hard I try.

I honestly don’t know how we’re paying for Christmas this year. I told my husband that we’re going to have to limit gifts to 5 per child. He thinks that means five big gifts. I told him this year is not the “Barbie jeep” kind of year. Last year we bought our daughter one of those Power Wheels Barbie jeeps and she hardly drives it. My plan for Christmas this year, is to sit down with sales ads and write a list of exactly what the kids are getting, and then go out the day after Thanksgiving to buy the things that are on deep discount. We’ll do the remainder of the shopping throughout the month of December, but will not deviate from the list. We can’t. We can’t afford it.

I’ve also been looking into Once a Month Cooking, or at least once a week; buying and cooking in bulk and freezing meals. Anything I can do to simplify my life and decrease our variable expenses (like groceries.)

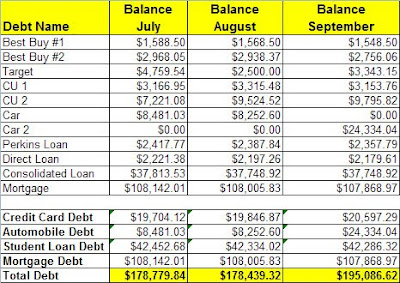

Here is our snapshot of our outstanding balances after paying all bills for the month of September.

My husband and I have been arguing about what exactly a budget it. He doesn’t seem to grasp the concept. He thinks that you can’t budget because “little things pop up” and I’ve told him repeatedly that the point of a budget is that those little things don’t pop up. He’s not talking about emergencies; he’s talking about wanting to go out on weekly shopping trips for non-necessities, like books, like clothes, like toys. As long as he thinks that a budget is supposed to be busted by these “little things that pop up” we will never get on track financially, no matter how hard I try.

I honestly don’t know how we’re paying for Christmas this year. I told my husband that we’re going to have to limit gifts to 5 per child. He thinks that means five big gifts. I told him this year is not the “Barbie jeep” kind of year. Last year we bought our daughter one of those Power Wheels Barbie jeeps and she hardly drives it. My plan for Christmas this year, is to sit down with sales ads and write a list of exactly what the kids are getting, and then go out the day after Thanksgiving to buy the things that are on deep discount. We’ll do the remainder of the shopping throughout the month of December, but will not deviate from the list. We can’t. We can’t afford it.

I’ve also been looking into Once a Month Cooking, or at least once a week; buying and cooking in bulk and freezing meals. Anything I can do to simplify my life and decrease our variable expenses (like groceries.)

Here is our snapshot of our outstanding balances after paying all bills for the month of September.

Subscribe to:

Comments (Atom)