We received our application and paperwork to refinance our home this weekend. The news was even better than I had expected as they are dropping our PMI from nearly $60 per month to less than $18.

By time all is said and done, with the lower interest rate, lower PMI, and lower taxes, as well as a longer mortgage term, we will be saving about $225 a month, which will initially be applied directly to our credit cards and later will be either saved or applied towards principle. It all depends what is going on with the housing market when that time comes. If we're staying put, we'll need to pay five years off our loan. If we're leaving, we'll be saving towards a 20% downpayment to prevent PMI on the next home.

Monday, April 30, 2012

Monday, April 23, 2012

A Little Early

I may have celebrated a little too early last week. As it turns out, if you include my 401k loan, I am still over $200,000 in debt. However, I did pay off more than $700 in debt this month, and that includes what we charged for our vacation.

Yay, right!? Okay, so I know we shouldn’t have charged our vacation, but I know that my husband is getting a bonus this month and another in three months, so we’ll be able to pay it off by summer. I know we would be further ahead if we had just not taken a vacation, but we enjoyed ourselves and it was really good for us to get away as a family.

But we have gotten some good news and some “good” news in the past couple of days that may bode well for our financial future as it relates to our house. I called my current mortgage lender about refinancing and found out that I can refinance to 4.5%, as opposed to the current 6.0%. There are about $2400 in fees, including appraisal, credit report, closing costs, etc. This will lower our monthly mortgage payment about $140 a month. Because I currently have PMI on my home, they will not let me reduce my mortgage term from 30 years to 15 or 20 years. I’m not sure of the logic of this, aside from the fact that it keeps me paying PMI longer. It doesn’t matter though, because I’m going to continue paying the same amount towards my mortgage to pay my principle off quicker and ultimately get out of PMI quicker.

The other “good” news, that I put in parenthesis because it’s not really good news, but it’s better than the alternative, is that we received word on our appeal of our property value. They decreased our property value 25% for 2010, and 5% for 2011, so we should be receiving a refund of overpaid property taxes and will be paying less going forward.

The combination of these two items means we will likely see a nearly $200 decrease in our monthly mortgage payment. While we’re still stuck in a home that we hate, the extra money means that we can pay off our debt faster.

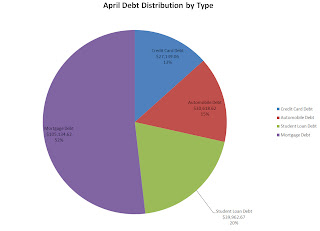

And finally, here is our current debt picture.

Yay, right!? Okay, so I know we shouldn’t have charged our vacation, but I know that my husband is getting a bonus this month and another in three months, so we’ll be able to pay it off by summer. I know we would be further ahead if we had just not taken a vacation, but we enjoyed ourselves and it was really good for us to get away as a family.

But we have gotten some good news and some “good” news in the past couple of days that may bode well for our financial future as it relates to our house. I called my current mortgage lender about refinancing and found out that I can refinance to 4.5%, as opposed to the current 6.0%. There are about $2400 in fees, including appraisal, credit report, closing costs, etc. This will lower our monthly mortgage payment about $140 a month. Because I currently have PMI on my home, they will not let me reduce my mortgage term from 30 years to 15 or 20 years. I’m not sure of the logic of this, aside from the fact that it keeps me paying PMI longer. It doesn’t matter though, because I’m going to continue paying the same amount towards my mortgage to pay my principle off quicker and ultimately get out of PMI quicker.

The other “good” news, that I put in parenthesis because it’s not really good news, but it’s better than the alternative, is that we received word on our appeal of our property value. They decreased our property value 25% for 2010, and 5% for 2011, so we should be receiving a refund of overpaid property taxes and will be paying less going forward.

The combination of these two items means we will likely see a nearly $200 decrease in our monthly mortgage payment. While we’re still stuck in a home that we hate, the extra money means that we can pay off our debt faster.

And finally, here is our current debt picture.

Wednesday, April 18, 2012

Milestone!

I input all of the payments we've made this month, as I do after every pay day. I put all of our new balances in, taking into account what we spent on vacation. The only outstanding payment we have for April is my car, but I can estimate the balance based on interest rates and fixed payment amounts.

And then I came to a shocking and exciting realization.

For the first time since I started my debt payoff journey, we owe less than $200,000 in debt!

This months debt total is $199,564.32!

Slow and steady wins the race, right?

In other news, I'm trying to refinance our house. Supposedly, HARP 2.0 eliminated a cap on LTV and appraisals on your home. As I am learning, this is not necessarily so. Since financial institutions have a choice in whether they want to offer HARP refinancing or not, most of them are not willing to provide refinancing through this program. Why should they, I guess, when they're making a profit off of those of us that are locked into high interest rates and haven't walked away from our homes yet.

I tried to refinance through my credit union yesterday, but they enforce a 125% LTV cap on their HARP loans. We're looking at closer to 148% based on Zillow's values. Even if we used the higher assessment we received from the auditors office for tax purposes, we're still at 133% LTV.

I hate that we live in a society where I'm being punished for being responsible and paying my mortgage, unlike the majority of my neighbors. I don't know if our situation would be more bearable if we were paying less on our home, but it would certainly lessen the sting. Every day I ask myself why we're still paying our mortgage when all of our neighbors have walked away and the current owners paid 1/3 of what we did for our home. We're gluttons for punishment, I guess.

We have to make a pretty big repair to our home, to the tune of over $8000, but I don't know where we're going to find the money. In better times, we might have been able to take out a home equity line of credit, but since our equity is negative, there is nothing to take out. It's our sewer line, and it's a ticking time bomb. The walls are cracked and it has started to shift in about 1/4-1/2 of an inch. I know we need to fix it, but I don't know where we'll find the money.

Roto Rooter was pretty shady about the whole thing; they told us in our home that it would be a max $4000 to have the work done, so I took a $4000 loan out of my 401k, only for them to give us a proposal of $8175. When I told him he had quoted us $4000 at our home, he said there was no way he would have quoted that because it was impossible and told me to take out a loan for the other $4000. I told him I took out a loan for the first $4000 and it wasn't even in the ballpark of what we were willing to do for our home at this time.

I applied for a new job too. I'm not sure if I am ready to leave where I am, but the job I applied for pays significantly more, and it's more in line with the career path I'm following. We'll see if I even get an interview, and then I will start making decisions if it's necessary.

Alas, I must get back to work, but I wanted to share my good news.

And then I came to a shocking and exciting realization.

For the first time since I started my debt payoff journey, we owe less than $200,000 in debt!

This months debt total is $199,564.32!

Slow and steady wins the race, right?

In other news, I'm trying to refinance our house. Supposedly, HARP 2.0 eliminated a cap on LTV and appraisals on your home. As I am learning, this is not necessarily so. Since financial institutions have a choice in whether they want to offer HARP refinancing or not, most of them are not willing to provide refinancing through this program. Why should they, I guess, when they're making a profit off of those of us that are locked into high interest rates and haven't walked away from our homes yet.

I tried to refinance through my credit union yesterday, but they enforce a 125% LTV cap on their HARP loans. We're looking at closer to 148% based on Zillow's values. Even if we used the higher assessment we received from the auditors office for tax purposes, we're still at 133% LTV.

I hate that we live in a society where I'm being punished for being responsible and paying my mortgage, unlike the majority of my neighbors. I don't know if our situation would be more bearable if we were paying less on our home, but it would certainly lessen the sting. Every day I ask myself why we're still paying our mortgage when all of our neighbors have walked away and the current owners paid 1/3 of what we did for our home. We're gluttons for punishment, I guess.

We have to make a pretty big repair to our home, to the tune of over $8000, but I don't know where we're going to find the money. In better times, we might have been able to take out a home equity line of credit, but since our equity is negative, there is nothing to take out. It's our sewer line, and it's a ticking time bomb. The walls are cracked and it has started to shift in about 1/4-1/2 of an inch. I know we need to fix it, but I don't know where we'll find the money.

Roto Rooter was pretty shady about the whole thing; they told us in our home that it would be a max $4000 to have the work done, so I took a $4000 loan out of my 401k, only for them to give us a proposal of $8175. When I told him he had quoted us $4000 at our home, he said there was no way he would have quoted that because it was impossible and told me to take out a loan for the other $4000. I told him I took out a loan for the first $4000 and it wasn't even in the ballpark of what we were willing to do for our home at this time.

I applied for a new job too. I'm not sure if I am ready to leave where I am, but the job I applied for pays significantly more, and it's more in line with the career path I'm following. We'll see if I even get an interview, and then I will start making decisions if it's necessary.

Alas, I must get back to work, but I wanted to share my good news.

Subscribe to:

Posts (Atom)