Our debt headed the wrong direction in a big way last night. We bought a new car. A brand new car. Ultimately, it was the right decision. I need to keep telling myself that, because the new car payment makes me want to scream and throw myself off of a building, but it was a necessity.

A little over a month ago, we were told that our car had a rusted out cross member. We were quoted between $5-6k to fix it. We owed $8000 on the car. And it was only worth $5500 in trade. We looked at the numbers, tried to figure out what our best option was, and ultimately decided that we needed to get a new car. We wanted to keep the payments as close to our existing payments as possible, which meant $288 a month. After walking into several dealerships and being told that it was an impossibility for a new car, we started revising our numbers. After looking at our actual payment (we were paying on a biweekly basis) and realizing we were actually paying $313 a month, and seeing that our gas mileage would be cut in half with the new car, saving us about $50 a month (maybe more) in gas, I set our ceiling at $350 a month.

We were still being quoted in the $360-$370 range though, so I told my husband that we should wait until next month and see if there were any other incentives, lower interest rates, or Labor Day sales. I thought, when I left work yesterday, that we were waiting to buy a new car. However, one of the guys that we had been talking to called and told my husband that he could get us into the car we wanted for $350 a month, so we went up tot he dealership. Of course, we got there, and he told us the lowest he could go was $367. So, my husband decided to play hard ball and called the other dealership that we had visited and they said they could beat that. So the dealership we were at said they could go to $365, taking a loss on the car, and they would throw in the free Homelink mirror and oil changes for a month. The other dealership said they could beat that, and the men at the dealer we were standing in were irritating me anyway.

My husband decided that $2 was worth driving to the other dealership. I told him there was no way we were going back to the first dealership if we left. We got tot he second dealership and they quoted us $367 with no Homelink and no free oil changes. After buying Gap insurance because of the negative equity we were rolling into our loan, we ended up with a $378 a month car payment (nearly $30 more than my ceiling) for less of a car. I was, and still am, pretty irritated.

Ultimately, I know that we were lucky to get a new car for less than $400 a month. We are lucky to be out of the money pit that was our old car and we're lucky we got $5500 on it, given everything that was falling apart. I'm just angry that we could have got the car we really wanted, for less, at the first dealership, but my husband wanted to haggle over $2 and we ended up paying even more. I can tell you, when I buy my car (not the family car), I'm doing all of the talking and I'm deciding which car we buy.

I plugged the numbers into my debt snowball calculator and discovered that it will take a year longer to pay off this car than it would have taken to pay off our old car. With a 3.9% interest rate, by paying it off early, we'll be saving quite a bit of interest. Our old car loan was at 6.75%, so I don't feel so bad about the 3.9%. It's better than what either of our credit unions could have given us.

I'm just sucking hard on that $378 a month car payment.

Looking at the numbers, I hope it works out the way it looks on paper and we are only paying about $15 a month more for car ownership than we were, but that only works if the car gets the mileage they say it does.

I also made a decision that a lot of people will probably disagree with this morning. I stopped deductions from my paycheck for my 401(k). As I see it right now, I'm looking at negative return on investment consistently. I felt like I was throwing good money after bad, and feel like, after about six months of applying my 401(k) deductions to credit cards, we'll be in a better place financially so I can start contributing again. Right now, I just really want to get out of this debt that is plaguing us so I can stop worrying about making our monthly bills all of the time.

I put in a call to our mortgage company last week and they haven't called me back, so I'll have to follow up with them today. I also contacted my credit union to see if they happen to refinance upside down loans. I'm trying to streamline our finances as much as possible. It will relieve a lot of stress in the long run.

Tuesday, August 31, 2010

Monday, August 23, 2010

Day 72: Small Changes

I can not believe we are 72 days into trying to dig our way out of this mess. The days just blend together, and it feels like we're making no progress. I know we're making progress, because the numbers are obviously going down, but it's such small progress that it almost feels pointless.

I got our monthly statement for the Target card, which we transferred half the balance from. It was kind of disheartening to see that the minimum payment was still over $100 and we still paid $88+ in interest. I know they use an average daily balance method for computing interest, so we still paid interest on the huge balance for a third of the month, but it was a little discouraging. The fact that the minimum payment only went down $28 was kind of discouraging too. Hopefully September's statements give us a much better picture of what our new monthly payments will look like.

I got some advice about our mortgage, so I'm going to have to contact our lender this week to discuss some refinance or modification options with regards to our loans and the governmental programs that are in place. It looks like our mortgage is held by Fannie Mae, which opens up some new options for us. It looks like one of the options allows up to a 125% LTV refinance option, but it only makes sense if there aren't astronomical fees associated with it.

And one of the biggest things that has happened to help our financial picture? My husband quit smoking. He's going on day five without a cigarette. Eliminating that expense will make a pretty substantial ($350-$400) difference to our budget, not to mention he will be healthier and the kids won't see him smoking. He's angry with me right now, because of the way he quit smoking, but hopefully in the future he will realize that I only did it because I love him, and the good reasons (health, kids) weren't working, so fighting about money did. If he's healthier in the long run, I think I can deal with him resenting me for now.

I got our monthly statement for the Target card, which we transferred half the balance from. It was kind of disheartening to see that the minimum payment was still over $100 and we still paid $88+ in interest. I know they use an average daily balance method for computing interest, so we still paid interest on the huge balance for a third of the month, but it was a little discouraging. The fact that the minimum payment only went down $28 was kind of discouraging too. Hopefully September's statements give us a much better picture of what our new monthly payments will look like.

I got some advice about our mortgage, so I'm going to have to contact our lender this week to discuss some refinance or modification options with regards to our loans and the governmental programs that are in place. It looks like our mortgage is held by Fannie Mae, which opens up some new options for us. It looks like one of the options allows up to a 125% LTV refinance option, but it only makes sense if there aren't astronomical fees associated with it.

And one of the biggest things that has happened to help our financial picture? My husband quit smoking. He's going on day five without a cigarette. Eliminating that expense will make a pretty substantial ($350-$400) difference to our budget, not to mention he will be healthier and the kids won't see him smoking. He's angry with me right now, because of the way he quit smoking, but hopefully in the future he will realize that I only did it because I love him, and the good reasons (health, kids) weren't working, so fighting about money did. If he's healthier in the long run, I think I can deal with him resenting me for now.

Tuesday, August 17, 2010

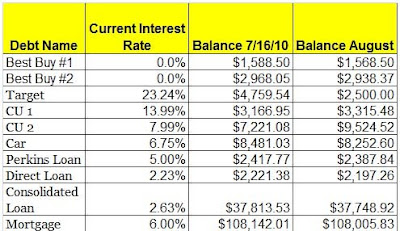

Day 66: This Month's Picture

{kind=link}

Here is our debt picture today, August 17.

Overall, we've paid our debt down $340.52 in the past month, and $1288.25 since I started keeping track in June. The bad news is that our credit card debt has actually gone up $142.25 in the past month.

My husband and I had a not so pleasant discussion on the state of our financial affairs tonight. I'm extremely unhappy with his $400 a month cigarette habit.

We were denied the refinance. We would need to refinance 112% LTV and the refinance plan only allows up to a 110% LTV, so we have to pay another $4000 off of our principal, or our house value needs to increase (which it won't) in order to be eligible for a refinance. That means that now, we're going to have to find a way to come up with an additional $85 a month for our mortgage payment, which is going to be hard to do when we're already running a $1000 a month shortfall. I know that can't be entirely accurate, because our credit cards only went up less than $150 this past month, and I don't see any week where we can't meet our bills over the coming month, there's just no extra money.

I think I'm going to look into a second job this week, see if I can pick up something in retail through the holidays, if anybody is even hiring. At least knowing that it's temporary will help me get through the days/nights. If we can get one credit card paid off, it will help our financial position immensely.

Wednesday, August 11, 2010

Day 55 Continued: A little good news

I got a call from my credit union. They were not able to give us the full amount we were requesting for the credit limit increase, however they were able to to raise the limit to $10,000 and we transferred $2000 of the balance from the Target card, leaving us with $2733.75 on the Target card, and a $9,420 balance on the credit union card. They're also lowering my interest rate to 7.99%, so I lost a percentage point. My credit score was 740, so I am feeling pretty good right now.

We're trying to decide if we try again for a personal loan for the other $2700 so we're not paying anything to Target. If not, we'll just throw the rest of our money at that outstanding balance and get it paid off. Transferring a little more than 42% of the balance will help decrease the amount of interest we're paying on the Target card, so it will give a little extra to go towards principal.

Now, we just need the mortgage company to give us a call back. Fingers crossed.

We're trying to decide if we try again for a personal loan for the other $2700 so we're not paying anything to Target. If not, we'll just throw the rest of our money at that outstanding balance and get it paid off. Transferring a little more than 42% of the balance will help decrease the amount of interest we're paying on the Target card, so it will give a little extra to go towards principal.

Now, we just need the mortgage company to give us a call back. Fingers crossed.

Day 55: Just Waiting for Answers

The past five days have been filled with activity.

Yesterday, we met with the mortgage broker to discuss refinancing our house. We were going over the numbers, he discussed a FHA refinance program, and the noticed that our loan was actually conventional. I had thought it was FHA too, but apparently not. He also thought that the sellers had paid our down payment, when in reality, there had been no down payment.

We talked numbers, he asked what houses were selling for in our area, I told him I wasn't sure but that Zillow had our house valued at about $95,000. Its weird, because the house right next to ours is built exactly the same, except that they added a bonus room to the back, and it's at $105,000 on Zillow. The bonus room only added an addtional 100 square feet. Anyway, I told him that we've had at least four foreclosures on our house, and that if he'd called us two months ago, our value was sitting at closer to $105,000, but in the past two months we've lost about $10k on the value of our house because three of those foreclosures sold at less than $40,000 each. That's been since the first of June.

He gave us two different possibilities and is looking into which one will work for us. If he's able to refinance our conventional loan under the FHA program, we won't need an appraisal and we'll need to show up to closing with $1500 to start our escrow account. We'd close the end of September and not have an October mortgage payment, so it's completely feasible. If we can't do the FHA refinance, then we'll have to do the Fannie Mae refi, which involves an appraisal. I'm not sure if our house will appraise high enough to refinance that way or not. It may, because our house is the second highest valued on the street, according to the auditors office and Zillow, but it may appraise lower because of cosmetic things that we simply haven't had time to fix, like the fence our neighbors ran through, the hole in the wall behind our front door where my son slammed the door handle into it, and the crack in the ceiling above our shower. I do know that if we have to have an appraisal, I will probably be painting the bathroom sooner, rather than later, to get rid of the peeling paint and border.

He should be giving us a call back in the next two days. Regardless, both options make our monthly payment about $50 less than what we're paying now, and $138 less than our new payment that will go into effect on October 1, so we'll be better off financially. I figure that if we are able to refinance, I will continue to pay that additional $50 towards our principal, so our payment will stay the same.

I forgot to mention, the mortgage lender will also be paying all closing costs for either option, including the appraisal fee if we need one. We only have to come up with the escrow amount. It won't actually cost us anything additional.

The other thing that I have been looking in to, and am waiting on a response regarding, is a credit limit increase and balance transfer. I already struck out with my husband's credit union, but my credit union has always been a lot more likely to work with us.

For example, my husband's credit card through his credit union has a $3500 credit limit and a 14.99% interest rate. It's been the same credit limit for years and years and years. When we applied for the credit limit increase, instead of giving us a reduced amount, they offered us a fixed term personal loan.

My credit card through my credit union started with a $5000 limit and a 13.99% fixed interest rate. I called this past January for a credit limit increase. They increased my limit to $7500 and asked if I would be interested in moving the balance to an 8.99% variable rate card and told me that, if at any point in the future, it looked like interest rates were moving so high that the variable rate card was no longer a good option, we could always move it back to the fixed rate card. I called them on Monday and asked how long it would be before I could apply for a credit limit increase for the sole purpose of a balance transfer.

The loan officer told me, "Usually, it is between six months to a year, however you have a very extensive history with us and an excellent payment history, so we may be able to reconsider you now. Let me get this to one of our underwriters and I will give you a call back". I love, LOVE that they look at my entire history with them and not just how much total debt I have. Even if they can't give me an increase, which I kind of expect, I'll still be singing their praises because they looked at more than just our astronomical debt when I told them that we're trying to transfer a balance from a 24% interest card.

So today, I just get to sit and wait, and see if I get good news from either company. If we were able to refinance and do the balance transfer, we'd probably be saving close to $100 a month in interest, maybe more. That's money that would be going directly towards paying off the principal amounts.

On a side note, our mortgage broker mentioned the fact that they're building a casino near our house. He said that he expects to see property values increase once it's built and they start to improve the area around it and suggested that in the next two to three years, we check our property values and consider moving, if it's feasible. We had already told him that we wanted to move in probably five years, so it was nice to get that bit of info from him. Of course, by then interest rates will probably be sky high, but we'll see.

Yesterday, we met with the mortgage broker to discuss refinancing our house. We were going over the numbers, he discussed a FHA refinance program, and the noticed that our loan was actually conventional. I had thought it was FHA too, but apparently not. He also thought that the sellers had paid our down payment, when in reality, there had been no down payment.

We talked numbers, he asked what houses were selling for in our area, I told him I wasn't sure but that Zillow had our house valued at about $95,000. Its weird, because the house right next to ours is built exactly the same, except that they added a bonus room to the back, and it's at $105,000 on Zillow. The bonus room only added an addtional 100 square feet. Anyway, I told him that we've had at least four foreclosures on our house, and that if he'd called us two months ago, our value was sitting at closer to $105,000, but in the past two months we've lost about $10k on the value of our house because three of those foreclosures sold at less than $40,000 each. That's been since the first of June.

He gave us two different possibilities and is looking into which one will work for us. If he's able to refinance our conventional loan under the FHA program, we won't need an appraisal and we'll need to show up to closing with $1500 to start our escrow account. We'd close the end of September and not have an October mortgage payment, so it's completely feasible. If we can't do the FHA refinance, then we'll have to do the Fannie Mae refi, which involves an appraisal. I'm not sure if our house will appraise high enough to refinance that way or not. It may, because our house is the second highest valued on the street, according to the auditors office and Zillow, but it may appraise lower because of cosmetic things that we simply haven't had time to fix, like the fence our neighbors ran through, the hole in the wall behind our front door where my son slammed the door handle into it, and the crack in the ceiling above our shower. I do know that if we have to have an appraisal, I will probably be painting the bathroom sooner, rather than later, to get rid of the peeling paint and border.

He should be giving us a call back in the next two days. Regardless, both options make our monthly payment about $50 less than what we're paying now, and $138 less than our new payment that will go into effect on October 1, so we'll be better off financially. I figure that if we are able to refinance, I will continue to pay that additional $50 towards our principal, so our payment will stay the same.

I forgot to mention, the mortgage lender will also be paying all closing costs for either option, including the appraisal fee if we need one. We only have to come up with the escrow amount. It won't actually cost us anything additional.

The other thing that I have been looking in to, and am waiting on a response regarding, is a credit limit increase and balance transfer. I already struck out with my husband's credit union, but my credit union has always been a lot more likely to work with us.

For example, my husband's credit card through his credit union has a $3500 credit limit and a 14.99% interest rate. It's been the same credit limit for years and years and years. When we applied for the credit limit increase, instead of giving us a reduced amount, they offered us a fixed term personal loan.

My credit card through my credit union started with a $5000 limit and a 13.99% fixed interest rate. I called this past January for a credit limit increase. They increased my limit to $7500 and asked if I would be interested in moving the balance to an 8.99% variable rate card and told me that, if at any point in the future, it looked like interest rates were moving so high that the variable rate card was no longer a good option, we could always move it back to the fixed rate card. I called them on Monday and asked how long it would be before I could apply for a credit limit increase for the sole purpose of a balance transfer.

The loan officer told me, "Usually, it is between six months to a year, however you have a very extensive history with us and an excellent payment history, so we may be able to reconsider you now. Let me get this to one of our underwriters and I will give you a call back". I love, LOVE that they look at my entire history with them and not just how much total debt I have. Even if they can't give me an increase, which I kind of expect, I'll still be singing their praises because they looked at more than just our astronomical debt when I told them that we're trying to transfer a balance from a 24% interest card.

So today, I just get to sit and wait, and see if I get good news from either company. If we were able to refinance and do the balance transfer, we'd probably be saving close to $100 a month in interest, maybe more. That's money that would be going directly towards paying off the principal amounts.

On a side note, our mortgage broker mentioned the fact that they're building a casino near our house. He said that he expects to see property values increase once it's built and they start to improve the area around it and suggested that in the next two to three years, we check our property values and consider moving, if it's feasible. We had already told him that we wanted to move in probably five years, so it was nice to get that bit of info from him. Of course, by then interest rates will probably be sky high, but we'll see.

Friday, August 6, 2010

Day 50: The Downs and The Ups

Yesterday was not a good day. We got a notice from our mortgage company that, after rebalancing our escrow account, we're running $595.06 short for the year. We also had an increase in property taxes due to a school levy, and an increase in homeowners insurance premium due to a sewage back up in our basement that resulted in a nearly $10,000 claim. So, after adding the increased taxes, premium, and shortage and dividing it over the next twelve months, our mortgage payment was going up $85 a month. That might not seem like a lot to some, but it's enough to put us over our heads and ultimately result in us falling behind on our mortgage.

If it weren't for the massive minimum payments on our maxed out credit cards, we wouldn't have a problem with paying our mortgage, even with this increase. We have got to find a way to get out from under our Target credit card and it's 24% interest rate. For ever $135.00 minimum payment, $96+ is going towards interest. We tried applying for a credit limit increase with my husbands credit union last month, so we could do a balance transfer. They countered with an offer for a private loan with a 10.74% interest rates, but the monthly payments would have been over $400 a month. We're trying to reduce our payments, not triple them.

Yesterday, the mortgage broker that we went through to buy our house called my husband. He left him a voicemail about reducing our interest rate on our house, and subsequently reducing our minimum payments. I've been looking at refinancing for several months, because right now we're in a 6% fixed interest rate on a 30 year mortgage, which almost seems criminal with the historic low interest rates we're seeing at the moment. But here's the thing; we owe over $108,000 on our house. According to Zillow, our house is only worth $95,000. Every refinance offer I've looked at has required a down payment of 5% minimum. We don't have any money for a down payment, we don't have money for closing costs or fees associated with refinancing, and we're not sure how long we're staying in the house anyway. The refinance offer I was looking at last night required a 5% down payment to refi, and would have taken 14.5 months to recoup the costs associated with the refinance.

However, the notice from our mortgage lender yesterday was enough to push us into action. My husband called the mortgage broker back last night and left a message for him to give us a call. The worst that can happen is he can offer us nothing, right? I contacted our insurance company to see what impact raising our deductible to $1000 will have on the premium for our car, and for our house. I don't think we can change the deductible for the house mid-term, but I want to see what the different rates are with our current provider because I'm going to shop around. I hate to, because I've been a customer for 13 years, but we just can't afford to pay any more than necessary. I work for an insurance company and would get a 15% employee discount if I switched, but I still don't know if it will be low enough to replace our current company. I'm going to give my credit union a call this morning to see about a credit limit increase/balance transfer from our high interest card. I've gotten a pretty decent raise since our last credit limit increase. And if we can transfer the balance, we're going to have to cut up our Target card. just get rid of it. It's a toxic card.

The good is, my husband got his bonus this morning. I wasn't expecting it until next month. The bad? It's 8:30 am and the bonus is gone. I paid our past due cable and electric bills and the Target bill that's due next week. At least we're current though. As long as we can keep current, we'll be ok. I see a garage sale in the near future. If I'd known my neighbors were having a garage sale today, I would have probably taken the time off work to have one myself. Oh well, hindsight is 20/20.

I think my husband is finally seeing how much we're struggling. Not enough to quit smoking, but enough that he's planning to start rolling his own cigarettes as a cost saving measure. Hopefully that will transition to quitting altogether in the near future.

If it weren't for the massive minimum payments on our maxed out credit cards, we wouldn't have a problem with paying our mortgage, even with this increase. We have got to find a way to get out from under our Target credit card and it's 24% interest rate. For ever $135.00 minimum payment, $96+ is going towards interest. We tried applying for a credit limit increase with my husbands credit union last month, so we could do a balance transfer. They countered with an offer for a private loan with a 10.74% interest rates, but the monthly payments would have been over $400 a month. We're trying to reduce our payments, not triple them.

Yesterday, the mortgage broker that we went through to buy our house called my husband. He left him a voicemail about reducing our interest rate on our house, and subsequently reducing our minimum payments. I've been looking at refinancing for several months, because right now we're in a 6% fixed interest rate on a 30 year mortgage, which almost seems criminal with the historic low interest rates we're seeing at the moment. But here's the thing; we owe over $108,000 on our house. According to Zillow, our house is only worth $95,000. Every refinance offer I've looked at has required a down payment of 5% minimum. We don't have any money for a down payment, we don't have money for closing costs or fees associated with refinancing, and we're not sure how long we're staying in the house anyway. The refinance offer I was looking at last night required a 5% down payment to refi, and would have taken 14.5 months to recoup the costs associated with the refinance.

However, the notice from our mortgage lender yesterday was enough to push us into action. My husband called the mortgage broker back last night and left a message for him to give us a call. The worst that can happen is he can offer us nothing, right? I contacted our insurance company to see what impact raising our deductible to $1000 will have on the premium for our car, and for our house. I don't think we can change the deductible for the house mid-term, but I want to see what the different rates are with our current provider because I'm going to shop around. I hate to, because I've been a customer for 13 years, but we just can't afford to pay any more than necessary. I work for an insurance company and would get a 15% employee discount if I switched, but I still don't know if it will be low enough to replace our current company. I'm going to give my credit union a call this morning to see about a credit limit increase/balance transfer from our high interest card. I've gotten a pretty decent raise since our last credit limit increase. And if we can transfer the balance, we're going to have to cut up our Target card. just get rid of it. It's a toxic card.

The good is, my husband got his bonus this morning. I wasn't expecting it until next month. The bad? It's 8:30 am and the bonus is gone. I paid our past due cable and electric bills and the Target bill that's due next week. At least we're current though. As long as we can keep current, we'll be ok. I see a garage sale in the near future. If I'd known my neighbors were having a garage sale today, I would have probably taken the time off work to have one myself. Oh well, hindsight is 20/20.

I think my husband is finally seeing how much we're struggling. Not enough to quit smoking, but enough that he's planning to start rolling his own cigarettes as a cost saving measure. Hopefully that will transition to quitting altogether in the near future.

Thursday, August 5, 2010

Day 49: Figured it out, I think

I think I've figured out the discrepancy in the Average Daily Balance and the payoff amount. All of these purchases are on interest deferred payment plans. Although we're not paying interest, and won't as long as the balances are paid off in a timely fashion, however, the interest is still accruing and is being included in the average daily balance.

I already intended to pay off these purchases before the payment period expired, however realizing that I'm accruing interest on top of interest on top of interest that is deferred has ensured that I will NOT pay these off late. I might even make sure I pay each of these off a month early so there is no way they can charge me the deferred interest.

We keep talking about having a garage sale to clear out our house and make a little money. I think it's time to stop talking and just do it. As long as our minimum payments stay as high as they are, we're never going to get out from under these credit cards. We'll make progress one month, and then as soon as something pops up, we'll be back under again.

I'm having a hard time getting my husband to stick to this too. He texted me yesterday and asked if it was ok to buy $30 worth of books. I felt like saying, "Well honey, we paid our cable bill late and I've got a medical bill in collections. Do you think it's a good time to spend $30 on books?" Instead, I just responded with, "It's probably not the best time."

He wants to crack down on things that are fairly insignificant, like buying necessities at Aldi, but doesn't want to cut the biggest money wasters, like his smoking, or buying books. This past weekend he wanted to go shopping for clothes for the kids because he wanted to get out of the house. We still have a few months until we have to worry about buying winter clothes, or at least one month. My point is, it's not a necessity.

I've cut down on little things too, but it doesn't seem to matter. For example, I used to stop and get breakfast every day at McDonalds on my way to work, easily $5.50 a pop, and then I'd go out for lunch at $8.00+ a day. Now, I stop in the morning and get a parfait and a Diet Coke ($2.08), and I bring a Lean Cuisine for lunch ($1.98) for a savings of $9.44 per day. Multiply that by five days a week and I'm saving us nearly $50 a week on food alone, or about $200 a month. Our grocery bill is a little higher, but not $200 a month higher.

My husband should get his bonus from work next month. That will help, to be able to dump $500 into one of our credit cards. It will at least bring the minimum payment down a bit.

I already intended to pay off these purchases before the payment period expired, however realizing that I'm accruing interest on top of interest on top of interest that is deferred has ensured that I will NOT pay these off late. I might even make sure I pay each of these off a month early so there is no way they can charge me the deferred interest.

We keep talking about having a garage sale to clear out our house and make a little money. I think it's time to stop talking and just do it. As long as our minimum payments stay as high as they are, we're never going to get out from under these credit cards. We'll make progress one month, and then as soon as something pops up, we'll be back under again.

I'm having a hard time getting my husband to stick to this too. He texted me yesterday and asked if it was ok to buy $30 worth of books. I felt like saying, "Well honey, we paid our cable bill late and I've got a medical bill in collections. Do you think it's a good time to spend $30 on books?" Instead, I just responded with, "It's probably not the best time."

He wants to crack down on things that are fairly insignificant, like buying necessities at Aldi, but doesn't want to cut the biggest money wasters, like his smoking, or buying books. This past weekend he wanted to go shopping for clothes for the kids because he wanted to get out of the house. We still have a few months until we have to worry about buying winter clothes, or at least one month. My point is, it's not a necessity.

I've cut down on little things too, but it doesn't seem to matter. For example, I used to stop and get breakfast every day at McDonalds on my way to work, easily $5.50 a pop, and then I'd go out for lunch at $8.00+ a day. Now, I stop in the morning and get a parfait and a Diet Coke ($2.08), and I bring a Lean Cuisine for lunch ($1.98) for a savings of $9.44 per day. Multiply that by five days a week and I'm saving us nearly $50 a week on food alone, or about $200 a month. Our grocery bill is a little higher, but not $200 a month higher.

My husband should get his bonus from work next month. That will help, to be able to dump $500 into one of our credit cards. It will at least bring the minimum payment down a bit.

Subscribe to:

Comments (Atom)